A Message From The Chair

More Value, Less Cost

I’m excited to be your 2016 chair and look forward to moving the association forward ina positive direction. I’ve been blessed to have an extremely energetic board and a proactive management association, led by Kylene and her team.

I’m excited to be your 2016 chair and look forward to moving the association forward ina positive direction. I’ve been blessed to have an extremely energetic board and a proactive management association, led by Kylene and her team.

We’ve been tackling the dual goals of cutting costs and increasing benefits. You should start to see some of that in March when we launch five new online courses on our new learning platform. The new technology will provide an easier, higher-quality learning experience. You should also see fee reductions for IBBA education, online and in person.

We are focused on growing membership, with the goal of being 1,000 members strong by 2018. We’re going to be aggressive in making that happen. To that end, I hope you’ll be part of our Mission and help us reach that goal by encouraging your colleagues to join the IBBA community. As we’ve seen multiple times now, great things do happen when we rally together.

Secret Sauce

I have always believed our member conferences are a key part of IBBA’s value proposition, and the spring event should prove even more worthwhile (a big thank you to our conference committee folks!) The spring conference is scheduled from May 2 to 7 in Orlando, Florida, with the theme of The Extra Degree – Fire Up Your Performance!

We have an amazing lineup of courses, thanks to our education committee, with the most workshops (16) we’ve had in several years. We’re also expanding the highly popular Mastermind Sessions—targeted small group discussions, designed for sharing best practices.

These sessions are just part of what I consider IBBA’s secret sauce. Whether you’re sitting at lunch, or networking after hours, you’ll find collaborative, open idea-sharing from brokers all over the country and around the world. You rarely find that kind of cooperative spirit at local meetings.

Your Insight

One last note, I’d like to thank everyone who took the Market Pulse survey. For the first time, we reached critical mass with over 348 responses. Success breeds success; the better our numbers the more the media will pick upon our results.

We’re also providing newsletter templates and presentation decks to members who participate so they can better leverage the Market Pulse Survey and differentiate themselves among their potential client base. This is the most accurate data in the market, and is only available to those who take the short survey. If you are interested in receiving this data, be sure to participate in the next Market Pulse Survey set to open in April.

Finally, if you have any idea of how to make IBBA better, call me at 920-436-9890 or email me at [email protected]. I appreciate those of you who have already reached out.

Continued Success,

Scott Bushkie, CBI, M&AMI

What Defines a Serious Business Buyer?

Individuals who desire to purchase an established small business must be well prepared before the search process begins. Well managed, profitable and successful businesses with a bright outlook for the future are in short supply and very high demand.

Individuals who desire to purchase an established small business must be well prepared before the search process begins. Well managed, profitable and successful businesses with a bright outlook for the future are in short supply and very high demand.

Business owners and business brokers alike have little patience and interest in wasting their valuable time with buyers who have not taken the appropriate steps to demonstrate that they are fully prepared to acquire a business.

How does a buyer define themselves as being a “serious” candidate and not a casual, curious, tire kicker? The goal of this article is to outline the steps that a business buyer should take in advance so that they can stand out and be recognized as a serious and credible buyer.

Preparing a business for sale takes considerable work on behalf of the business broker and seller. Just a few of the steps include valuing the business, preparing the Confidential Business Review (executive summary), and organizing all of the corporate, financial, and tax documents. For a buyer to be recognized as a serious candidate, they too have a similar process and work that needs to be accomplished prior to being in a position to venture in the marketplace and begin assessing business opportunities.

So, what makes a buyer a serious candidate?

1. Personal profile and resume

Construct a detailed personal profile and biography. Not only will the seller need to see this document but any bank requires this as well. A resume is just a starting place.

The document should cover the following questions:

- What is your education and work experience?

- Who will be buying the business? Just you, you and your spouse, a partner, an investor?

- Why you are interested in buying a business?

- What is your investment criteria?

- What transferrable skills do you possess that qualify you for managing the business?

- How will you will be financing the purchase of the business? If bank financing will be utilized, a prequalification letter should be included. How much money do you have for a down payment?

- What is your timetable to complete the acquisition?

- Who is your advisory team? Which attorney will be drafting the Asset Purchase Agreement and facilitating the closing? Do they have experience with business acquisitions?

- What are the contingencies for the business acquisition? Do you have to leave a current job?Do you have to secure funding from a partner or a bank? Do you have to relocate and sell a house?

How will the buyer be funding the purchase?

Buyers should be knowledgeable about the size of business they are qualified to purchase. Will the buyer be utilizing personal funds for the transaction or will third party financing be used? Most acquisitions (without real estate) require 25% of the purchase price as a down payment. (Funds needed for closing costs and working capital are often provided as part of the loan package and can be financed.)

Buying and selling a small business requires a two way exchange of information. The buyer should be ready to disclose the amount they can invest and have a detailed plan on how they will finance the entire transaction. The idea that the seller is going to finance the sale is not a plan and this type of buyer will be quickly dismissed. Business brokers can be a great source for recommendations on which lenders are appropriate and likely to finance the business they represent.

The buyer should have a current personal financial statement prepared. If bank financing will be utilized, the buyer should be clear on their borrowing capacity and have a lender prequalification letter in hand (a banker can prepare this in a matter of hours). Don’t expect the broker or business seller to provide complete access to sensitive and confidential business documents without receiving assurances that the buyer has the appropriate resources to either purchase the business outright or obtain a business acquisition loan.

What industry experience or transferrable skills does the buyer have?

The optimal situation is when the prospective buyer has direct industry experience. This is especially pertinent when bank financing will be involved. Obviously, every business is different and each will have unique requirements for successful ownership. For some businesses, the buyer may be able to satisfy this requirement by having related practical work experience or transferrable skills. Certain businesses may require licenses, certifications, or a particular expertise to operate. If the buyer does not possess these it will be critical to confirm that there is a manager or key employee that has these qualifications. In other situations, the business may be very specialized and a buyer lacking a critical credential will be disqualified from obtaining bank funding. These issues should be discussed early in the process as the business broker will need to determine if you are managerially qualified to operate the business.

What is the type of business the buyer is seeking and why?

A serious buyer has developed a detailed and concise “investment criteria” for the business they seek to acquire. Several investment criteria attributes will include the type of business, the industry, the geographic location, the size of business, and the price/value of the enterprise.

Serious buyers will focus on enterprises which are suited to their background and qualifications. A buyer who inquires about an industrial packaging distributer, a restaurant, and a custom millwork company will not be treated as a serious candidate. Having an investment criteria that relates only to “profitable businesses” without regard to the business type, industry served, geographic location, and size is a clear red flag that the candidate has not put the proper time into honing their acquisition objective.

2. Realistic expectations.

Successful entrepreneurs recognize that there is no such thing as a perfect company. Business ownership involves taking on some level of risk and acquiring a business is no different. Buyers who seek to purchase a business 100% free of any flaws will be searching for a very long time. There will be areas of improvement for every business and the buyer will have to make a decision as to which negative elements are acceptable and which ones are not. Buyers who are too risk adverse may just not be cut out for small business ownership and being an employee is a more suitable career objective. Additionally, buyers often fail to realize that there is a limited supply of great businesses for sale…those that have year over year revenue growth, excellent profits, and bright prospects for continued advancement. Many of these businesses sell for the full listing price and for these types of successful businesses, buyers should be careful when submitting an offer less than 90% of what it is listed at. Most of the time there are multiple buyers who are evaluating the business and those candidates who submit, either a low-ball offer or an offer with unrealistic terms attached, will be wasting the valuable time of all parties involved not to mention possibly burning a bridge with the business seller and eliminating themselves from consideration.

3. Ability to react quickly

A serious buyer is well organized, has done their research, and knows what they want and what they can afford. They are decisive and capable of moving through the process in a timely and methodical fashion. If a partner, spouse, or investor will be involved in the acquisition, these individuals are consulted with in advance and are in agreement with the defined objectives. If advisors will be assisting in the evaluation, the advisors are aware of the acquisition search and are on standby for their assignment.

A serious buyer should have an understanding of how businesses are valued in addition to a comprehension of the typical steps in the acquisition process. They are prepared with a list of well thought and detailed questions designed with the objective of determining if the opportunity meets their investment criteria. A serious buyer recognizes that a “quick no” is far better than a “slow no” and they tackle those elements from the outset that would disqualify the business from being acquired. Once the opportunity is qualified, a serious buyer is in a position to make a ‘realistic offer’ and provide a letter of intent or terms sheet. A professional support team has been identified for drafting the Asset Purchase Agreement and facilitating the transaction closing. Lastly, a serious buyer will understand the due diligence process and already have their checklist in place. Funding for the acquisition has been planned and money for an earnest money deposit is liquid and available.

4. Professional Communication

A serious buyer is honest, direct, and forthcoming. Now is not the time to be cagey, cute, or evasive. You want to convey at the earliest opportunity your investment criteria, time table, financial wherewithal and reasons for pursuing the acquisition. This type of communication will build a foundation for trust and honest dialog in the weeks ahead. One viable solution for a serious buyer is to retain a business broker to assist with the search and business qualification. This approach provides far better results than a haphazard approach of firing off requests for information on any business posted on-line that catches their fancy. The business-for-sale industry is not the real estate industry. There are no open houses. This is a highly confidential process where professionals are retained to protect the sensitive data on the business for sale. A buy-side broker is paid by the prospective buyer for the time, energy, and work that is generated on their behalf. They are compensated to produce results.

There is nothing worse than going through the myriad of steps in preparing a business for sale to find a buyer that is not properly prepared nor has gone through the logical thought, planning, and preparation for acquiring a business. I have outlined the information that a business broker and seller needs when qualifying a candidate as a serious buyer. In order to close a transaction all of this information is required so it best that the buyer come prepared with this data at the outset. Few parties in this arena, want to have their time wasted or patience tested. The bottom line is that when you find the right business, you are in a position to act and make a realistic offer. Successful businesses are few and far between and often receive multiple offers. Why should the business broker and seller invest time in you?

Michael Fekkes is a Senior Broker at Enlign Business Brokers in Nashville, TN. Michael is a Certified Business Intermediary [CBI], a member of the International Business Brokers Association [IBBA], the IBBA Communications Committee Chair, as well as a former business owner.

Michael Fekkes

Note Regarding IBBA Monthly Learning Webinars

We are pleased to report unprecedented interest in our recent monthly learning webinars! We know some of you have been frustrated lately by our current 100 seat capacity. The cost associated with increasing our attendance capacity is significant, and something we are weighing. As a reminder, access to all the webinar recordings is an IBBA Member benefit. As such, we must assess if this investment would be wise and prudent use of the association’s resources. We will continue to evaluate the situation and options.

IBBA University Announcement

Are you ready to become a Certified Business Intermediary (CBI)?

Don’t miss your chance to sit for the CBI Exam on May 7th 2016 in Orlando Florida.

To register for the exam, check the CBI Exam box when registering for the 2016 Spring Conference.

Please contact [email protected] with questions regarding eligibility.

Connect + Collaborate = Close

It’s often just the one extra degree in life and business that separates the good from the great.

The IBBA’s Spring Conference brings you the education, skill development, best practice sharing and networking you need to fire up your performance this year!

• WORKSHOP SPOTLIGHT •

With 16 workshop offerings, there truly is something for everyone at this year’s Spring Conference! Workshops are included in your Conference pass!

- Steps to Building a Lucrative Franchise Resale Practice – Eric & Robin Gagnon

- 12 Keys to Success for Main Street Brokerage – Len Krick

- Business Buyers in the Digital World: How to Identify Them, Attract Them, and Convert Them – Bob House

- M&A vs Mainstreet: Size Does Not Matter. What Makes an M&A Deal? – Mike Adhikari

- Education as a Selling Tool – Doug Robbins

- The Top 5 Reasons a Loan Request is Declined & How To Avoid Them – Steve Mariani

- A Structured Seller Interview: The Key to Your Success as a Processional Intermediary – Carl Grimes

- The 10 Laws of Communication – Matt Sadati

- Using Retirement Funds as a Source of Equity in a Business Purchase – Suzy Granger

- Intimidate or Be Intimidated – Doug Robbins

- Deferring Gains and Reducing Tax Liabilities for Your Seller – Dr. Bart Basi

- Beyond the Numbers: Identifying the True Value Drivers that Will Tell You If Your Listing Will Sell & For How Much -Randy Bring

- Using Immigration and Business Brokerage: How to Expand Your market Overseas – Jessica Baines

- Leveraging Technology To Do More Deals – Clint Fiore

- Main Street Marketing Boot Camp – Len Krick

- The Basic Legal documents to Seal the Deal – Roman Basi

REGISTER BY MARCH 20th TO SAVE $100!

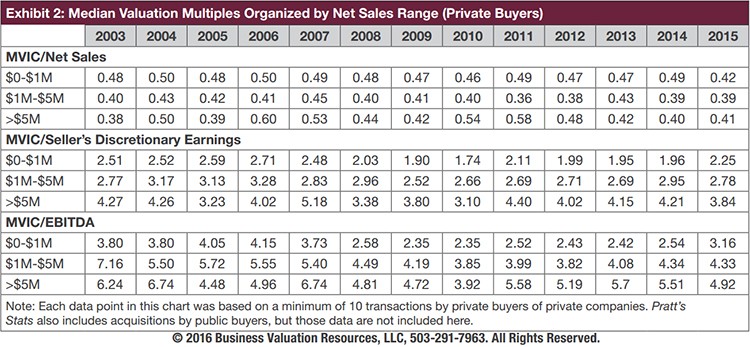

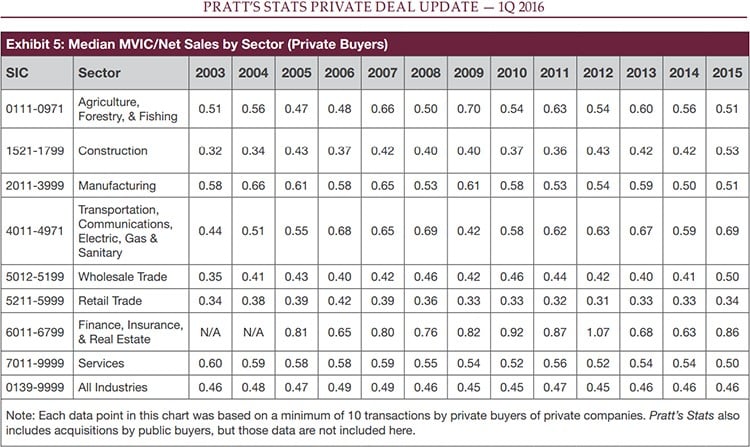

The information provided below is excerpted from the

Pratt’s Stats Private Deal Update: 1st Quarter 2016, which is copyrighted by and available exclusively from Business Valuation Resources, LLC. Brokers who contribute transaction details to

Pratt’s Stats on closed business sales receive the complete Private Deal Update plus three months of free access to the database for each deal included in Pratt’s Stats.

The quarterly Pratt’s Stats Private Deal Update (PDU) provides general trend information on valuation multiples and profit margins for transactions in the Pratt’s Stats database, available exclusively through Business Valuation Resources, LLC (BVR) at www.BVMarketData.com.

Financial advisors, merger and acquisition professionals, business appraisers, business brokers, investment bankers and many others use the Pratt’s Stats database to determine the value of their subject company by applying the market approach with comparable company data.

Pratt’s Stats is the premier source for private business purchase details and includes both private and public buyers with over 150 data points that highlight the financial and transactional details of the business sales. As of the publication date, the

Pratt’s Stats database contains 17,292 transactions in which the buyer was a private party. The database includes over 24,350 transactions in which a privately held company was sold to either a private or public buyer.

The charts and graphs presented below display median values.

MVIC: Total consideration paid to the seller and includes any cash, notes and/or securities that were used as a form of payment plus any interest-bearing liabilities assumed by the buyer. The MVIC price includes the non-compete value and the assumption of interest-bearing liabilities and excludes (1) the real estate value and (2) any earn-outs (because they have not yet been earned, and they may not be earned) and (3) the employment/consulting agreement values.

International Business Brokers Association – IBBA

Members who submit completed transaction information receive a three-month complimentary subscription to Pratt’s Stats, for each included deal, as well as a complimentary subscription to Pratt’s Stats Private Deal Update, a quarterly publication analyzing private company acquisitions from the Pratt’s Stats database. Pratt’s Stats collects private business transactions of main street businesses from business brokers, as well as from middle market M&A advisors where a public company purchases a private company. The Pratt’s Stats database is updated monthly with an average of 100 transactions. Pratt’s Stats users enjoy:

- Easy searching that identifies comparable transactions by keyword, revenue range, industry name, SIC code, profitability margins, company name, and more

- Hard-to-find data on how deals are structured including payment terms, purchase price allocations, employment agreements, non-compete agreements, private company financial statements, private company financial ratios

- Valuation multiples that point to the greatest value drivers

- The ability to track market pricing trends via Pratt’s Stats timely deal updates

- Access to payment term information including contingency payment and transaction fee details

- Asking price vs. selling price comparisons for spread analysis

- Listing date and selling date inclusions for timeon-market analysis

For more information about Pratt’s Stats, contact Doug Twitchell at [email protected], Adam Manson at [email protected], or Mitchell Cameron at [email protected] or visit www.BVResources.com/ Contribute to learn more.

Pratt’s Stats – Financial Details on 24,350+ Business Sales

As a key stakeholder in the transfers of private businesses, you know how crucial comparable business data is to pricing your clients’ companies. Pratt’s Stats, published by Business Valuation Resources (BVR) and featured in Inc. Magazine and the New York Times, contains detailed financial information on 24,350+ acquired private companies.

BVR invites you to submit your closed transaction details to Pratt’s Stats, the leading private company transaction database. In exchange you’ll receive complimentary access to: 1) all financial and transaction data in the Pratt’s Stats database, 2) a subscription to the Pratt’s Stats Private Deal Update™, and 3) use of the new, time-saving tool, Pratt’s Stats Analyzer™. You can submit confidentially—we won’t disclose any information you do not wish to.

3 Easy Steps to Submit

- Register online at: bvmarketdata.com/contribute

- Gather your closed transaction deals and login

- Click on “Submit Deal” and complete the form (you can also submit closed transactions via fax/email). If you have a larger quantity of closed transactions to submit (100+), a BVR representative will travel to your office (free of charge) to review and enter the deals!

Submit Your Closed Transaction Details and We’ll Give You:

- 3 months of FREE access to Pratt’s Stats for EACH closed transaction you submit that’s included in Pratt’s Stats

- Pratt’s Stats Private Deal Update – a quarterly analysis of private company acquisitions by private buyers from the Pratt’s Stats database

- Use of the Pratt’s Stats Analyzer – a time saving tool to help you more easily and quickly analyze the sales you find in your searches

- Listing in BVR’s referral directory – used by sellers and buyers searching for intermediaries

- Chance to win an iPad Mini for EACH closed transaction you submit that’s included in Pratt’s Stats. The more sold deals you submit, the more entries you receive into our quarterly drawing.

Don’t wait – submit your transactions today and reap the rewards!

For more information, please contact:

Mitchell Cameron or (971) 200-4837

The 7 Habits of a High Volume Broker Office – The 6th Habit: Compiling Your Memorandum

What buyers look for in your listing and why lenders read your memorandum!

A complete and comprehensive memorandum is not only a great advertising tool for buyers but also lenders will use much of the information included in them for their internal write ups. Countless times we are asked about small print items in the memorandum that we didn’t even know were there.

It’s typically that the first item a potential buyer receives after signing an NDA with the listing broker is a confidential memorandum. The next thing they do with it is share that with their trusted advisor and/or lending professional for a second opinion and validation of their research. Below are the initial items that both will review and depend upon when considering an offer on your listing.

First they look at the SDE or cash flow of the business to determine if it truly fits their requirements and is able to produce an acceptable level of income. This is where they typically ask about the “addbacks” and the validity of each one. Going item by item to better understand what is being presented as “seller discretionary” expenses. Some potential buyers will begin to lose interest at this point if they become overwhelmed by the amount of add backs used to meet their required income. The “unwritten” rule of thumb amongst most lenders is that if over 20% of the SDE is being derived by addbacks then this may be of concern. Keep in mind that items like depreciation, interest and owners salary and not really looked at by lenders as addbacks as they are basically included in almost every financing opportunity a lender considers. The biggest concerns come when they are multiple salary addbacks (other than owner), many cell phones, auto expenses, etc. that compile the majority of SDE. I won’t go into much more detail on addbacks as that is another writing entirely. You get the idea.

The second area a potential buyer explores is usually the current management and operational structure of the business. They want to understand what it takes to manage this business and who is doing which job today. Will there be employee concerns in this area after the transaction closes and will employees be difficult to replace if they do leave. The buyer also tries to understand, in these earlier stages, where they fit in and where their skillset is of greatest value. If the company has been lacking in sales and marketing and this particular buyer has that strength then in their mind they see all upside and this usually increases their level of interest. This is a big step toward considering an offer on this business.

At this point they understand the cash flow and havedetermined where they can be of value to the company so what do they read next in your memorandum? The current customer base and competition is the next area we usually see them explore. They look for customer concentration concerns and competition in the market. From a lending perspective we can understand that an older, more established business might gravitate to one or more customers that have increased their purchases over the last many years.

This may lead to a customer concentration concern but, if for example, one of your customers is GM and they have increased their orders over the last 10 years, is that truly a bad thing?

Although GM has now become 45% of their sales, it shows the level of quality and customer service this selling company provides. I interpret that as a natural event and present it as such with the lenders we work with. I explain that any quality company would do the same and turning GM work down would be a poor management decision. Maybe the company is guilty of not diversifying, but as the principals grow older this tends to be less of a concern to them, completely understandable and explainable. By explaining the lenders view on the customers it usually brings the concern to a minimum with a potential buyer and keeps them moving forward.

Although GM has now become 45% of their sales, it shows the level of quality and customer service this selling company provides. I interpret that as a natural event and present it as such with the lenders we work with. I explain that any quality company would do the same and turning GM work down would be a poor management decision. Maybe the company is guilty of not diversifying, but as the principals grow older this tends to be less of a concern to them, completely understandable and explainable. By explaining the lenders view on the customers it usually brings the concern to a minimum with a potential buyer and keeps them moving forward.

Competition can be understood 2 different and opposite ways. I have actually had a lender decline a loan due to the LACK of competition. Their concern was that the town only had one of these type stores and that it was not a viable business model, they went on to say that they would have preferred 4 or 5 competing stores in the market that would have shown sustainability. I prefer to present a business that owns market share and even a specialized niche’, but again, this will depend on a lenders perspective and understanding. The buyer is usually looking for an opportunity to capitalize on their competition and your memorandum should disclose potential growth avenues. A few weaknesses of the competition will confirm the opportunity to a buyer.

Detail some growth and expansion possibilities moving forward in addition to the competition described above. Providing just enough information to allow the buyer to understand 2 or 3 growth opportunities is a must to include. Don’t go into too much detail as they sometimes interpret that as a sales pitch (which is really what the entire memorandum is) but leading them with possibilities allows them to explore growth potential in a direction you may want. If a buyer feels the avenue for growth is there it leads them to believe the future is in their hands and after all, isn’t it?

The goal of every memorandum is to leave the reader with a feeling that they would be missing an opportunity if they don’t act now. Effort upfront will pay big dividends in the end.

Stephen Mariani is the President and Founder of Diamond Financial Services. Stephen has owned 7 previous businesses and has been an entrepreneur since 1983. He has mastered SBA SOP rules and regulations and has become an “expert” in SBA loans.

IBBA Magazine

IBBA Magazine