IN THIS ISSUE:

Letter From The Chair

Barry J. Berkowitz, PhD, CBI, M&AMI

As we head into the second half of this tumultuous year, it’s a good time to take stock. This is typically the time I take inventory of the goals I originally set, measure my progress, and determine where and how I need to make adjustments in order to achieve my goals by year’s end.

As we know, this year, so far, is anything but ‘typical.’ I can tell you the goals I personally set for myself as IBBA Chair, for my business, and for my personal life frankly have been obliterated and simply won’t materialize. I’m guessing many are experiencing the same. So now what do we do?

We can either dwell on all the things that won’t be, or we can set new goals and focus on what can be. And I believe the IBBA is setting a good example of how to do the latter. Here is what I see:

No live Conference? Ok, instead we went virtual and delivered over 70 hours of training content and peer sharing. You can still purchase the Virtual Conference Pass to tap into all the recordings, thru July 31.

No Main Street Vendor Marketplace? Ok, instead we will build a Vendor Directory to release September 1 so you can find and connect with solutions providers online, all year round.

No Member Excellence Awards Ceremony? Ok, instead we hosted some virtual Happy Hours with our recipients so we could celebrate their success, share stories and jokes, and enjoy each other’s company.

Prolonged travel concerns? Ok, instead we’re ramping up our distance learning with the newly released online course #145 Effective Business Packaging; actively working on 3 more online courses; planning a virtual Summit for late summer; and discussing a virtual mini-symposium for the Fall.

We also invested in our infrastructure by updating the IBBA website and upgrading our IBBA University platform, and went back live with our newly-renamed podcast, IBBAinsights.

So, the key question is, and always has been, what CAN you do?

Holding yourself up against your beginning goals will likely not be a productive endeavor. So, set some new goals that are challenging but realistic for the remainder of the year, stop looking in the rear view mirror at that might have been, and set your sights on what can be.

For my part, I’m going to relish my remaining six months as Chair of this organization that I’m just so grateful to be a part of. I’m tweaking my business model, marketing and processes to incorporate things I learned from the Conference. And I’m going to cherish, even more, time with my wife and cats.

So, to all my colleagues, keep your chins up and press onward.

Barry J. Berkowitz, PhD | CBI, M&AMI | Berkowitz Acquisitions | [email protected]

Building a Small Business Pipeline

Lou Vescio, CBI, M&AMI

Every successful Business Broker advertises services to an expansive list of businesses to build a brand and source deals. The first step in building this pipeline is to determine what types of businesses the broker wants to sell and in what geographical area the broker wants to work. The goal should be to build a pipeline to increase the Broker’s probability of success.

Finding “good” businesses to sell and taking them to market is one of the most difficult tasks for a Business Broker, and this an especially difficult task for a new Broker. So, what are “good” businesses, and how can a Broker find them?

A good business can be defined as follows:

- The business has a history of solid sales revenue, preferably increasing revenue.

- The business has a history of positive cash flow, preferably increasing cash flow.

- The business has a motivated owner that wants or needs to sell his business.

In order to build a pipeline of good businesses to sell, we need to create or acquire a list or a database of businesses that have a high probability of meeting the above requirements.

Sales Revenue

Private companies are not required to divulge their sales to the public, but we have companies like Sales Genie that do a somewhat satisfactory job of predicting revenues for small businesses. Sales Genie lists about 15.4 million businesses. Another source is the D&B Hoovers’ company database which also provides similar information, and other lists are available.

Determining a successful business by sales revenue range varies significantly depending on the business segment. For example, PeerComps (www.peercomps.com) shows the average limited service restaurant that has $500,000 in sales will generate a 22% DE ($110K) and will sell for 2.74 times DE (about $300K).

By comparison, a car wash that has sales of $500K will generate a 40% DE ($200K) and will sell for 3.5 times DE (about $700K). Two different businesses with the same sales but significantly different cash flows and values.

Cash Flow

There is no way to know the cash flow of a particular company when we purchase a database, but depending on the industry, we can predict what the average cash flow should be for a given industry with a certain amount of sales. PeerComps and other sold databases provide excellent information if the Broker takes time to analyze a specific industry. Whether the Broker is a generalist and works ten or more industries, or a specialist by choosing to work in one or two industries, we can predict average cash flows for an industry based on sales revenues.

Motivated Seller

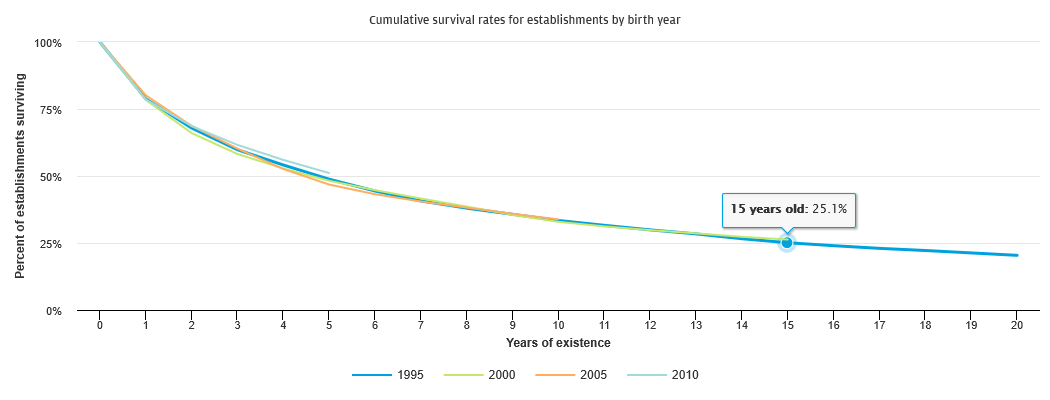

A Seller may be motivated to sell for several reasons, some of which are good reasons and others of which are not so good. Ideally, we want a motivated seller that has been successful over a long period of time. The chart below from the US Bureau of Labor Statistics suggests only 25% of small businesses make it to 15 years of longevity, implying that such businesses have a higher probability of success. Businesses that have been around for 15 or more years have managed to survive at least one recession and have a higher probability of having an owner nearing retirement, a good motivation for selling.

It should also be noted that database firms like Sales Genie also report how many years the company has been in business.

How to Build the Database

For a generalist Broker, the first step of building a good pipeline is to select about 10 different industries that have a high probability of selling. The Business Brokers Press (https://businessbrokeragepress.com) frequently lists the top 10 businesses purchased in a recent period. The January 2020 list included the following list, and the Broker should develop his/her own Top 10 list based on personal experiences and interests.

Restaurants

Fast Food – Non-Franchises

Services Businesses

[/columns-container]

Construction Businesses

Auto Repair, Service & Parts

Convenience Stores

[/columns-container]

Distribution Businesses

Bars

Gas Service Stations

[/columns-container]

Service Franchise Resales

[/columns-container]

Once the list of the top ten industries is selected, purchase a database of at least 1,000 businesses in the desired geographical area. If the Broker only wants to sell businesses that will sell for $500K or more, PeerComps data will suggest the minimum sales required in each specific industry to only advertise to businesses that have a high probability of selling for $500K or more. In addition to the minimum sales level, only select businesses that have been in existence for 15 years or more. By making these selections, the broker will improve the probability of finding successful businesses with owners that are older and have positive reasons for selling, like retirement.

Lou Vescio, CBI, M&AMI | Coastal Business Intermediaries & Agency Brokerage Consultants

[email protected]

The Value Quandary of Selling an Existing Franchised Business

Emmet Apolinario, CEPA, CVB, Sunbelt Business Advisors

This article looks into the case of an existing franchised business that may not sell for more than the cost of opening a new start-up franchise.

In my years of helping business owners sell their existing, franchised businesses, we have been regularly approached to assist in determining the sale value of the franchised operation. It is common when discussing the potential sale value of an already operating franchise, that the sale value may end up being less than the cost of opening a new start-up operation.

We agree, there should be value proposition in selling an existing well-run franchised business. But what are the factors that determine the eventual selling price of this franchised operation?

An entrepreneur will open a new franchise start-up, operate, and run it for three, five and maybe even more year and then, for varying reasons, need to consider the sale of the business. That business may be a highly profitable business, or it may not.

It may be a business that struggled to get started and the owner have had to support it for years; it may be a franchised operation that from the start became profitable and in a short time became a financially rewarding operation. In most cases, starting this franchised business was not just a financial investment, it was a labor of love and dedication to pursue the entrepreneurial dream of the owner.

Whatever happened through the short or long years of owning this franchised business, the owner sustained and operated the business. But now, a decision to sell is imminent and the quandary is, “How much will this business sell for?”

A franchised business owner will reach out to us to assist them with the potential sale of the existing franchised operation. As experienced business brokers, I’m pretty sure you’ve participated in many of these franchise resales over the years. Using industry data, as well as regional and national comparables, you provided the business owner a probable selling price. If the business broker/intermediary or advisor was competent, trained, and in some cases certified in providing an “opinion value of sale,” an accurate and reasonable sale price was provided to the owner.

Eight times out of ten the probable selling price of the business startled the owner, and not in a good way. The franchised business owner often responded with, “How could that be? To purchase and open a new franchise would cost XXX dollars with zero revenue! I am an existing, operating, franchised business which has been operating for 4 plus years and I can only sell for $ XXX amount?”

Good News and Bad News

This is a common reaction from an existing franchised business owner.

My popular response to the franchisee is “Good news…and Bad news…”

Good news is that you are an existing business; you’ve weathered the tough times and you seem to be a sustainable business.

The Bad news? You are an existing business and your earnings and profits can now be benchmarked to show how profitable (or not) your franchised operation is.

Yes, the franchisee has revenue and profits to speak of, but what type of earnings and profits are brought in? Yes, they are a franchise. Yes, they now have a business history and track record of performance. That’s good. But the bad news we may have to bear is that the earnings and profits represent a factor where a multiple is applied to arrive at a sale value. Unfortunately, that sale value may not be the expectation of the franchisee.

Not Leveraging the Potential Value

Depending on the franchise concept or format, a new franchisee will extend the investment by acquiring additional territories. Over the years, I have heard franchisees exclaim, “I have 2 more territories that I have not opened yet…it’s worth this much.” My question when I hear that is, “How much did you pay for those additional territories?” The response is typically, “I purchased a 3-pack and received a territory discount by committing to opening 2 territories.”

The discussion inevitably led to, “That territory is worth $ xxx, if a buyer purchased such and such territory…” The fact is if a franchisee has this franchised territory for the last 4 years but did not open up another location, what kept them from opening the other franchised location(s) or why didn’t they expand into additional territory?

These are difficult discussions to have. The franchisee will either accept the fact that it was their fault and acknowledge that they did not leverage the value by adding locations, or they will come up with excuse after excuse. When the business is taken to market, there are no guarantees that the business buyer will agree with the franchisee’s philosophies and reasonings regarding the additional territories.

Will a business buyer, open to paying for those additional territories, be found? That’s where we wish we had a crystal ball, to foresee the future. I know every effort will be made to sell the business but given what I have seen over the last 17 years, this type of franchise business buyer is a very rare species.

In closing, as professional intermediaries, it is vital that we tell franchisees what they need to hear versus what they want to hear. This makes for an effective and honest relationship with your business seller clients.

Emmet Apolinario, CEPA, CVB | Sunbelt Business Advisors

[email protected]

Did Your Seller Prepare to Exit? If Not, Can You Help?

Lisa Riley, PhD, CBI, CM&AP, CBB| Delta Business Advisors

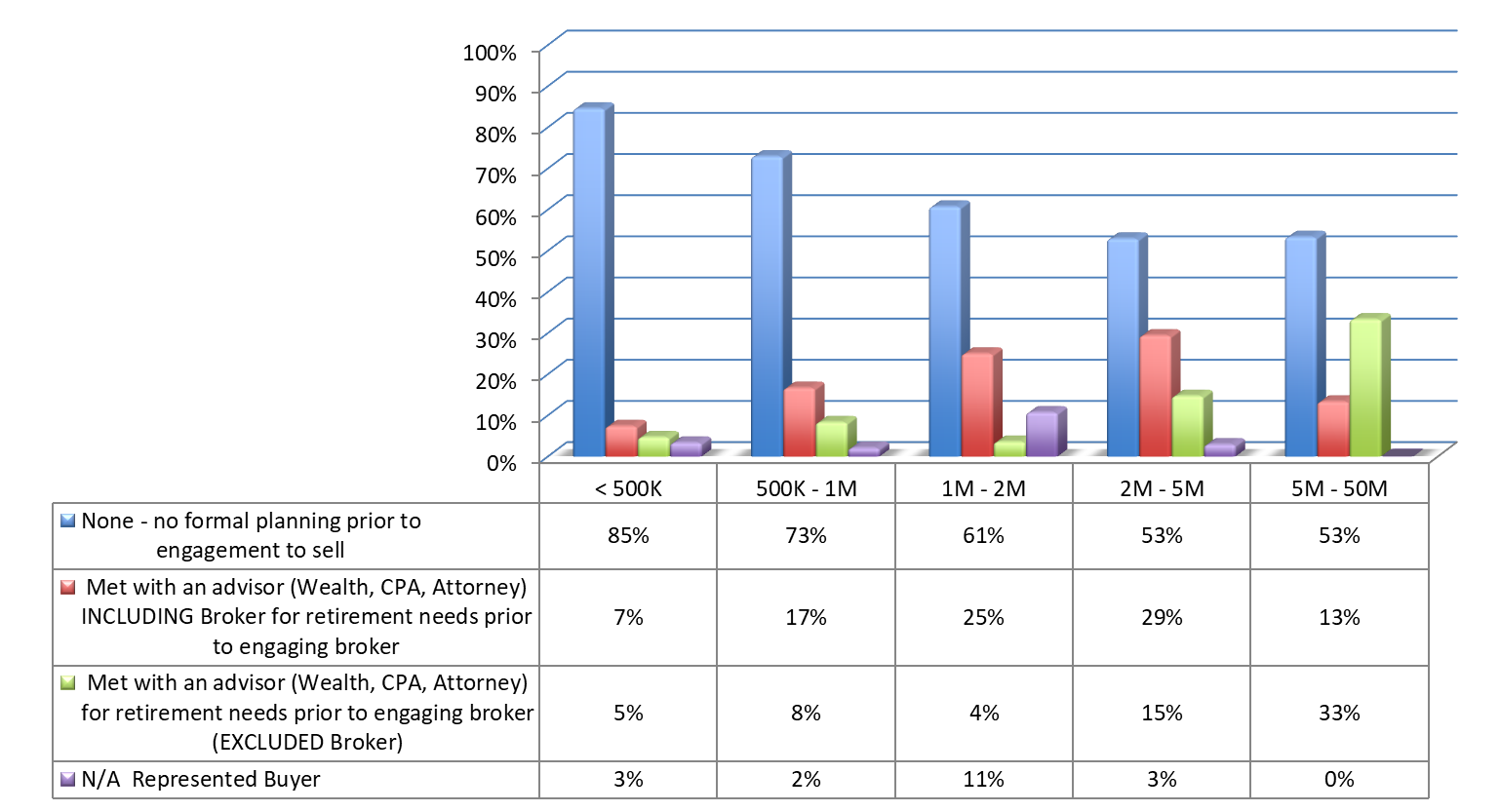

Every quarter, Business Brokers are asked a series of detailed questions about the businesses they sold the prior quarter. Since Q4 2017, intermediaries have reported on whether the Seller had any type of formal exit planning prior to engagement and the length of time they spent on exit planning prior to marketing the business for sale.

Of businesses that sold in 2020 Q1, most owners did NOT plan for their exit prior to selling their business. The vast majority reported that the Seller had no formal planning prior to engaging the Business Broker/Intermediary to sell. In fact, 85% of businesses which sold for less than $500,000 had not talked with anyone. Those with the most planning were in the Lower Middle Market, however more than 50% had not planned for their exit. On the other hand, almost half of Sellers in the Lower Middle Market (54% and 46%, respectively) had at a minimum discussed retirement/next step needs with an Advisor and/or Intermediary prior to Engaging in Selling their business.

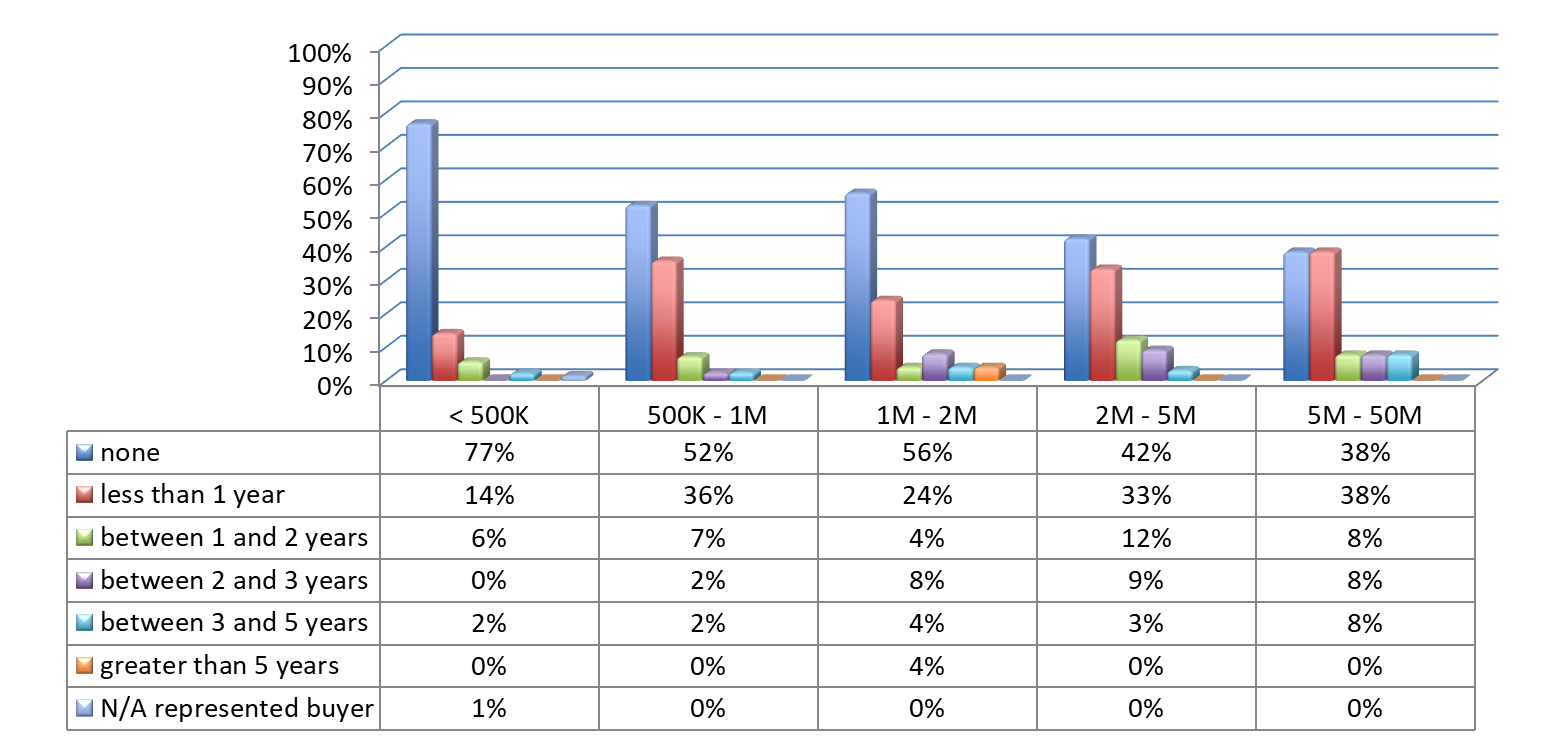

Exit Planning Preparation

Of the Sellers who do plan ahead, most are still moving through the exit planning process at a rapid pace, with less than a year between initial consultation and the Broker taking the Business to market. Only in the lower middle market, with businesses valued between $2 million and $50 million, do advisors report approximately 1 in 4 sellers (24%, each) planned more than 1 year prior to sale. That still means that 76% of business owners are leaving a multimillion-dollar event up to chance.

Amount of Exit Planning Prior to Marketing Business

In an ideal world, Brokers/Intermediaries want to connect with sellers three or more years ahead of a sale, especially in the lower middle market. That gives Sellers a reasonable amount of time to make meaningful changes to financial issues like working capital and separating the discretionary (e.g., Ferrari) expenses from true business expenditures. It is also about the minimum amount of time necessary for Sellers to develop key employees and shore up their leadership and/or management team, get their Advisory Team in place, and identify the tax consequences of the sale.

* The IBBA and M&A Source with the support of the Pepperdine Private Capital Markets Project and the Graziadio School of Business and Management at Pepperdine University has conducted quarterly Market Pulse Reports since Q2 of 2012 to gain an accurate understanding of the market conditions for businesses being sold in Main Street (values $0-$2MM) and the lower middle market (values $2MM -$50MM). For the most recent and prior reports, please go to: https://www.ibba.org/resource-center/industry-research.

Lisa Riley is the Owner and Designated Broker of Delta Business Advisors. Lisa is a Certified Business Intermediary [CBI], a Certified Business Broker [CBB], PhD, Chair of Market Pulse Committee and Board Member of the International Business Brokers Association [IBBA] and the Arizona Business Brokers Association [AZBBA], as well as a former business owner and university professor. She can be reached at 480-686-8062 or [email protected]. Delta Business Advisors is a boutique firm located in Scottsdale, AZ providing services for business transitions from valuation throughout the sales and transition process to final sale/exit or acquisition.

Dealing with Landlords During and Post COVID-19

Jeffrey D. Jones, ASA, CBA, CBI

When selling a business, obtaining a lease assignment, or getting a new lease for a property has always been a critical step in transferring business ownership interest. COVID-19 and the related pandemic restrictions imposed on businesses by various government regulations has further complicated the process. This article will address the historical process of working with buyers and sellers in dealing with landlords and the additional factors know complicating that process due to COVID-19 issues.

Part of a business broker’s job is to act as an intermediary between the buyer, seller, and landlord in transferring the business ownership and obtaining a lease assignment or new lease. The following is a summary of the steps that should be taken.

Step One – Upon getting a new listing, get a copy of the complete lease and related addendums. This is just as important as getting the business’s financial records.

Step Two – Read the lease to understand the terms and conditions specified in the lease.

Step Three – Send a letter to the landlord making them aware of your client’s interest in selling their business. Notify the landlord about the need for confidentiality and that no one should be contacting the landlord about the subject lease without approval from you or the tenant. Confirm the basic terms and conditions of the lease such as the remaining term of the lease, the current rental rate, future rent increases, and the availability of lease options. Ask for confirmation that there are no outstanding issues such as past due rent, equipment ownership issues, and/or needed repairs to the facilities. Ask what documents the landlord wants from the buyer such as a financial statement, a business plan, and resume. In getting a lease assignment, ask who is going to prepare the lease assignment, the landlord’s attorney or an escrow company. Find out if there is going to be a fee imposed by the landlord or the landlord’s attorney to prepare the lease assignment. If there will be a new lease, who will be preparing the lease.

Step Four – Once an earnest money contract is signed, send another letter to the landlord that specifies the date of closing, the effective date for the lease assignment or new lease, and include the landlord’s required documents from the buyer. Address any issues the buyer has with regards to the term of the lease, property condition issues, lease options, and/or rental rates. Historically, these issues have been addressed in a person to person meeting with the landlord or management company; however, COVID-19 issues has now limited personal contract and now has been replaced with conference calls, Zoom meetings, and/or emails.

Step Five – As part of the closing process, it is the broker’s job to ensure that the lease documents are signed at closing. It is likely the landlord will not release the original tenant from the lease and lease guarantee until the expiration of the base term of the lease. This should be discussed with the client seller at the time of listing the business, so there will be no surprises at closing. Finally, the broker should arrange for the signed lease documents to be delivered to the landlord for final approval.

Every lease will have Basic Lease Terms that include the location of the facility to be leased, size of the space being leased, the term of the lease, the rental rate, and the use of the facilities. Additional provisions will typically address the following issues:

- Common Area Maintence Fees

- Real Estate Property Taxes

- Real Estate Insurance Cost

- Utility Charges

- Trash Fees

- Merchant/Tenant Association & Related Fees

- Advertising Fees

- Sign Fees & Regulations

- Construction Cost

- Parking & Common facilities uses and restrictions

- Compliance with Laws & Safety Requirements

- Required Liability Insurance

- Regulation of Hazardous Materials

- Landlord Liens on business assets

- Landlord’s Rights of Access

- Restrictions regarding Lease Assignment & Subletting

- Lease Default Provisions

- Sales of Premises by Landlord

- Hours of business operations

- Security Deposit

- Holding Over Provisions

- Relocation Option

- Broker Fees

All of these provisions are somewhat negotiable when seeking a new lease. Landlord flexibility is usually a lot less when granting a lease assignment.

COVID-19 has put extra pressure on tenants and landlords with regards to re-negotiating existing lease terms, payment of past due rent, and changes buyers want to make to an existing lease or new lease upon the purchase of a business. Many small business owners are now several months behind in rent payments, particularly those businesses deem non-essential and required to close due to government mandates. Some business owners have gotten Paycheck Protection Program Loans and SBA Disaster Loans. This has raised the issues of loan forgiveness versus loans that will need to be repaid upon the sale of a business.

Surprisingly, it has been my experience thus far this year that buyer inquiries are actually up from the period prior to COVID-19; however, converting buyer interest to deal closings has been extra time consuming. Buyer prospects are looking for ways to reduce cost, especially if they are buying a business that has suffered lost profits due to COVID-19 issues. Buyer prospects are offering prices that are 15% to 30% below the asking prices even for businesses that were not significantly impacted by COVID-19 issues. Then many of these buyer prospects want rent concessions from the landlord that include seeking 2 to 3 months of free rent, and rent reduction for some period of time. I am hearing from my client sellers that their landlords have not been very responsive to requests for rent reduction. In some cases the landlords have been willing to give the tenant more time to catch up on their rent rather than foreclose on the lease, but the landlords have mortgages to pay and cannot afford to lower the rents which would jeopardize their mortgage and wipe out their return on investment. Many landlords are now having to negotiate with their mortgage companies for reduced payments or postponement of payments due to insufficient rental income.

For most small to midsize businesses, rent including triple net charges needs to be no more than 10% of gross revenue. Today, rents for relatively new businesses are running well over 20% of gross revenue which is a recipe for failure without some sort of creativity in negotiating lease terms. I have a deal now in escrow on a franchise auto repair business where the current rent is 30% of gross sales. The buyer proposed to the landlord a 50% rent reduction for the remaining 4 year term of the lease. The landlord refused the offer. He already has a tenant with a tenant personal guarantee on the lease. There is no motivation for the landlord to reduce the rent. As a result, the seller agreed to significantly reduce the purchase price and has agreed to subsidize the rent for the remaining term of the lease so that buyer gets a 40% rent reduction.

It appears that price reductions and rent reductions will be a major factor in negotiating future business sale transactions. Price reductions of 10% to 30% will be required to offset the negative aspects and uncertainty of COVID-19. Furthermore, lease negotiations with the landlord and/or the current tenant will be necessary to make deals happen. From a landlord standpoint, areas of negotiations include offering some free rent time, deferring several months of rent payments to the back end of the lease, or offering to lower the rent for some specified period of time. At the very least, asking landlords not to raise the rent over the current amount even though the lease may have automatic rent increases specified in the lease. Getting little or no concessions from the landlord may require the seller to offer creative financing alternatives to the buyer and/or offer to subsidize the rent for some specified period of time.

In general, change is what drives the business brokerage industry. When the economy is suffering from a significant down turn, employment layoffs spur people to consider buying or starting a business. When the economy is booming, entrepreneurs want to take advantage of the good time and start or buy a business. When there is a lot of uncertainty about the direction the economy is going, buyer activity may well continue, but deal closings will be delayed until there is some degree of certainty in the economy. I have seen this to some degree in every presidential election year where buyer interest is strong, but deal closings are delayed until the election is finalized. Now we have both COVID-19 issues impacting the economy and a presidential election year impacting deal transactions. Is this the best of times or the worst of times for the business brokerage industry? Guess we will have to wait until COVID-19 issues and presidential issues provide some certainty in the marketplace. In the meantime, we will have to get more creative in our deal negotiations in helping our clients and customers reach their goals.

Jeffrey D. Jones, ASA, CBA, CBI | President of Advanced Business Brokers, Inc. | [email protected]

IBBA Member Benefits

To get started with your FREE access, login to your IBBA Member Account to get access from each benefit partner:

Bizminer

Business Reference Guide Online

ValuSource

V-Rooms

Get Connected to the IBBA!

IBBA Magazine

IBBA Magazine