Letter From The Chair

This past quarter has been an exciting one for the IBBA, as we have wrapped up a record breaking Spring Conference, welcomed 34 new Certified Business Intermediaries (CBI), rolled out two new IBBA Member benefits, and are continuing to grow our membership.

This past quarter has been an exciting one for the IBBA, as we have wrapped up a record breaking Spring Conference, welcomed 34 new Certified Business Intermediaries (CBI), rolled out two new IBBA Member benefits, and are continuing to grow our membership.

The Spring Conference had a theme of “The Extra Degree”. The idea behind The Extra Degree is that one extra degree can take just plain hot water and make it boil, therefore creating steam, if you have enough steam you can power a locomotive. All it takes is The Extra Degree to move yourself and your business in a positive direction. The Board and allyAMC have been hard at work to keep the IBBA’s train moving forward, and I believe that we are off to a great start!

Thank you to everyone who helped and attended the Spring Conference in Orlando, Florida. The conference boasted record breaking attendance since the recession! I hope to see even more of you at the Fall Conference in Phoenix-Tempe, Arizona. I have seen some of the lineup and it is very impressive – trust me, you will not want to miss it!

Congratulations to our 34 new CBIs who completed and passed the CBI Exam at the Spring Conference. To congratulate you on this accomplishment, we would like to offer you a discounted invitation to the Fall Conference. The Fall Conference is something we don’t want you to miss – keep an eye out for the special offer coming your way.

I am very excited to announce that the IBBA has partnered with PeerComps and Business Reference Guide to bring IBBA Members two new benefits. With just these two new additions, the benefits well exceed the cost of membership ($799 vs. $449). Do your colleagues a favor and tell them to join the IBBA to SAVE money and be part of a great group of people.

Not only has the IBBA been hard at work to offer you two new benefits, but we have also been hard at work in releasing six new online courses to IBBAUniversity.org, our new online learning platform. With 11 courses now easily accessible online, I encourage you to take a moment to explore the courses and enroll in one that sparks your interest.

One last note, I would like to thank the Board and all of the committee chairs and volunteers. We have accomplished a lot through the first half of the year, and I am excited to see what a passionate group of people can accomplish in the 2nd half of 2016. I feel we are just getting started! With 754 current members, I have no doubt the IBBA can be 1,000 strong by 2018!

Finally, if you have any suggestions on how to make the IBBA better, call me at 920-436-9890 or email me at [email protected]. I appreciate those of who you have already reached out.

Continued Success,

Scott Bushkie, CBI, M&AMI

Why Businesses Do Not Sell

It would be nice to live in a world where every business for-sale was sold at top dollar. While there is no such thing as a perfect business free from all defects, there are a number of problems that can hinder a sale that could be remedied, if given enough time. This article lists ten of the reasons which are often cited as contributing factors in an unsuccessful sale or a completed deal for less than potential value. Business intermediaries need to be upfront with their seller clients, educating them on the challenges faced, and the likely impact that one or more of these issues will have on completing a successful transaction.

It would be nice to live in a world where every business for-sale was sold at top dollar. While there is no such thing as a perfect business free from all defects, there are a number of problems that can hinder a sale that could be remedied, if given enough time. This article lists ten of the reasons which are often cited as contributing factors in an unsuccessful sale or a completed deal for less than potential value. Business intermediaries need to be upfront with their seller clients, educating them on the challenges faced, and the likely impact that one or more of these issues will have on completing a successful transaction.

1. UNREALISTIC EXPECTATIONS

a. Valuation/Listing Price:

Arguably, the price a business is listed at is one of the critical elements to a successful sale. An owner’s emotional attachment to their business, coupled with an inexperienced business intermediary’s desire to obtain the listing and please the seller, can be a recipe for disaster. Overpricing a business will deter knowledgeable buyers from establishing communications. Additionally, it will be extremely difficult to defend the valuation when a business has been priced unrealistically. The typical outcome is that the listing will languish in the marketplace and recovery becomes more difficult. Once on the market for months on end at the wrong price, the process in re-pricing and re-listing creates a whole new set of challenges, the least of which is maintaining credibility.

b. Unrealistic Terms and/or Structure

Deal structure, asset allocation and tax management must be addressed proactively and early in the process. Often the Buyer and Seller place all of the focus on the sale price at the expense of the ‘net after-tax results’ of a business transaction. In most cases, a seller could achieve a deal that provides a greater economic benefit when an experienced Tax Attorney/CPA assists with structuring the transaction. In addition to structure there are a number of other issues that could be problematic, including:

- Seller insists on all cash at closing and is inflexible in negotiating other terms.

- The buyer’s unwillingness to sign a personal guarantee

- The lack of consensus on the Asset Allocation

- Seller insisting on only selling stock (typically with a C-Corp)

- Inability to negotiate equitable seller financing, an earn-out, or terms for the non-compete

2. PROFESSIONAL ADVISORS

For a successful sale to occur, a business owner must have the right team of advisors in place. An experienced mergers & acquisitions intermediary will play the most critical role – from the business valuation to negotiating the terms, conditions, and price of the sale as well as everything in between (confidential marketing, buyer qualification, etc). Aside from the M&A advisor, a business attorney who specializes in business transactions is critical. Once again, “who specializes in business transactions”. Any professional who has been in the industry for more than a year will be able to point to a transaction that has failed because the lawyer that was chosen did not have the specialized expertise in handling business transactions. Additionally, a competent CPA who is knowledgeable about structuring business transactions will be the third key role. While a business owner’s current legal and tax advisors may have the best of intentions in assisting their client with the business sale, if they are not experienced with mergers and acquisitions it would be highly recommended to evaluate alternatives. In some cases, there is one shot when an offer has been received and it is therefore imperative not to attempt to make a deal that is out of reach and impossible to complete.

3. DECREASING REVENUES/PROFITS

The majority of buyers are seeking profitable businesses with year-over-year increasing revenue and profits. When a business has a less stellar track record with varied results or possibly declining revenue and/or profits, complications with the business sale are likely to occur. Not only will decreasing profits and revenue impact the availability of third party funding but it will have a material impact on the business valuation. While buyers traditionally purchase businesses based on anticipated future performance, they will value the business on its historical earnings with the major focus on the prior 12-36 months. For those businesses which have deteriorating financials, the seller should be able to articulate accurate reasons for the decline. Both the lender and the buyer will need to obtain a realistic understanding of the underperformance to assess the impact it is likely to have on future results. In cases where the seller is confident that the decline was an anomaly and is not likely to repeat itself, structuring a component of the purchase price in the form of an earn-out would probably be necessary. In other circumstances, when there are two or more years of declines, the buyer and lender will question “where is the bottom?” and what is the new normal. In this situation, a decrease in valuation will be inevitable. Cash flow is the driver behind business valuations and business acquisitions. The consistency and quality of revenue and income will be one of the key focal points when assessing an acquisition. It all relates to risk. Those businesses with dependable recurring revenue generated from contractual arrangements will generally be in greater demand than businesses who produce income based on a project based model.

4. INNACURATE OR INCOMPLETE BOOKS

One of the most critical components to a successful business sale is for the business to maintain accurate, detailed, and clean financial statements that match the filed tax returns. Not only will these financial statements be the basis for the business valuation but they will also be the criteria for whether the business will qualify for bank transaction funding. Too often the business is managed as purely a lifestyle business that is focused only on short term owner compensation, without regard to building long term value. In these cases, the owner has taken very liberal personal expenses that may not be able to be added back when deriving the adjusted earnings. Given the importance these documents represent, a business owner should ensure that the books are professionally managed and up to date. Records that are messy, incomplete, out-of-date or containing too many personal expenses will only give prospective buyers and lenders reasons to question the accuracy of the books. Last but not least, businesses that have a ‘cash component’ will need to report 100% of this income for it to be incorporated in the valuation.

5. CUSTOMER CONCENTRATION

Businesses that have a handful of customers that produce a large percentage of the company’s revenues, will probably have customer concentration issues, especially if one client represents greater than 10% of sales. It is important for a business owner to recognize that a business which lacks a broad and diverse base of customers possesses a higher degree of risk for a buyer as the loss of any one of these large clients could have a material impact on the future earnings. As a result, customer concentration will have an effect on the valuation, deal structure, and salability of the business. Vendor and industry concentration can also pose complications when selling a business. Specialization can be a competitive advantage for a business and assist in winning contracts. However, this same narrow industry focus could be a detriment if it is perceived that the business does possess a broad supply chain and ample options to source products and materials.

6. THE OWNER IS THE BUSINESS

It is not uncommon for the owner to play a significant role in the operation and management of the business. This is particularly true with smaller enterprises. Where this situation can present a problem is when the owner is not only the face of the business but also deeply involved with all facets of the company – sales, marketing, operations, management, marketing, and financial. If there are no key employees and there are few written processes and procedures, the business lacks a dependable and repeatable work flow. When it becomes evident that the business cannot operate effectively without the owner’s hands on involvement and personal know-how, it becomes problematic. Of equal concern is the relationship the owner may have with the customers of the business. If the customer does business with the firm largely in part of the relationship with the owner, this situation will create customer retention concerns and possible transition problems when the business is being sold. In summary, buyers want a business that can operate independently from the current business owner.

7. THE OWNER(S) IS AGING AND HAS SLOWED-DOWN

It is not uncommon for a business owner to become complacent after running the company for an extended period of time. Becoming tired and lacking the previous ‘fire in the belly’ has a way of spilling over into the business fundamentals. The number of trade shows that the business participates in decreases, the travel and new customer sales calls that routinely took place on a daily basis in the early years, have been paired down. The investment spending on equipment upgrades, vehicle replacement or marketing programs have been cut back. Innovation has come to a grinding halt and the business is on auto pilot. The financials have luckily held steady but for how long? An owner who has become burnt out almost unavoidably transmits their lack of zeal and drive to their staff and clients in a number of subtle ways. The net result is the company’s performance slowly begins to deteriorate. Unfortunately, this situation can become even more pronounced when the owner finally makes the decision to sell the business and mentally checks out at the worst possible time. Transferring ownership can be viewed by some as a highly emotional process, and the decision to sell at the right time is often ignored until the issue is forced upon the owner (failing health, divorce, disability, etc.) and usually at a fraction of the former valuation.

8. INDUSTRY IS DIMINISHING OR THREATENED

Over the last two centuries there have been a number of industries that have developed and grown significantly. In this same time frame, many new industries have been created while others have become extinct. The future outlook for a given industry will have a direct impact on the valuation and marketability of the business during a sale. Businesses facing obsolescence or mired in a shrinking industry will face an uphill battle when it comes time to transitioning or selling the company. Maintaining a diverse offering of products and services that are relevant to the market, not just today, but also with an eye to the future, will enable a business owner to avoid this situation. Not only will this assist in mitigating the impact from declining sales but also demonstrate to a prospective buyer that the business has a clear path to grow in the future.

9. CHOOSING THE WRONG LENDER

From loan application approval to transaction funding is a process in business transactions that can take six weeks or more, that is with an ‘experienced’ business acquisition financier. Many deals have fallen apart during this time frame because the buyer became aligned with the wrong financial institution. There is nothing worse, for all parties involved, to find out four weeks into the process that either the loan terms previously promised were not correct or worse, that the bank underwriter declined the loan.

In the field of business acquisitions, not all banks/lenders are the same. There are conventional loans, SBA backed loans, and there are lenders that provide cash-flow based financing and others that only provide asset based funding. One bank may turn down a borrower for an SBA 7a loan while another institution will readily accept it. Every lender has its own unique and frequently modified lending criteria. Therefore, buyers need to ensure they are working with the right lender from day one, or valuable time is wasted causing the deal to be compromised, or lost to another, better prepared candidate. Buyers should consult with the business intermediary representing the sale to determine which lenders have reviewed and/or pre-approved the transaction for funding. Obviously, buyers who are prequalified from the start and verify that the bank’s lending criteria conforms to the type of businesses they are evaluating, will be the best positioned for a successful acquisition.

10. COMMERCIAL PROPERTY ISSUES

For some businesses the saying “location, location, location” cannot be more important to the value of the company. Typically, this will pertain to retail businesses. If the physical location is of major importance, the business buyer will seek assurances that they can either purchase the real estate or be able to sign a long term lease. On the flip side, the business could be located in a part of town that has fallen on hard times or could be located on the owner’s personal property, both situations necessitating that the business be relocated. Also, some businesses are not easily relocatablewithout affecting the current customer base. All of these circumstances add another layer of complexity to the transaction.

Additionally, the type and size of facility can also have a material impact on the sale. If the facility is not large enough to provide the enterprise a sustained growth path, a buyer could become disinterested. Another situation could be the value of the property. If the current owner purchased the land/building a decade or two earlier and the financials or recast do not reflect a current FMV rent/lease payment, valuation problems will occur.

Business transactions involving the sale of commercial real estate can be hampered by the Environmental Site Assessments (ESA’s) – Phase 1 and Phase 2. Property that is contaminated can be very costly to clean up and will have an impact on the closing. When this situation arises, it will be important for the buyer and seller to have a clear understanding of the costs to resolve the issue, which party is responsible, and whether a price offset will be warranted.

Other complicating factors involving commercial real estate include zoning changes that require a property to be brought up to new codes, and clear definition of who bears responsibility and the cost of this process. Last but not least, the agreement by the landlord with either a lease assignment or offering a new lease at comparable rates.

Summary

Most small business owners have spent the majority of their life building their business. It is not uncommon for a business seller to become so emotionally attached to the company that they look past some rather glaring problems that a business intermediary, a lender, or prospective buyer will immediately recognize. It is natural for a seller to want to obtain the highest price possible for their business. There is so much bad information on the web related to multiples and business valuations that this should not come as a surprise. M&A Advisors need to be honest and direct in educating a business seller on the challenges faced in a potential sale, the range for a realistic transaction price, as well as creative terms and structuring options that might be utilized. Beinga people pleaser and ignoring any potential problems will only provide the seller with unrealistic expectations. In the arena of business negotiations there are few if any “pleasant surprises”. Dealing with issues up front rather than late in the sales cycle process should be the golden rule.

Michael Fekkes

Did You Know? The CBI Recertification How-To

Once you have earned your CBI designation there are requirements to recertify every 3 years. A one-year extension can be requested in special circumstances.

The recertification requirements include a current individual or corporate membership with the IBBA or M&A Source, payment of the annual credentialing fee ($55), attendance of at least one IBBA conference and 48 credit hours of education, association activities, or completed business transactions.

These 48 credit hours are actually quite flexible. Did you know you will receive an additional 15 credits for each additional conference that you attend? Did you know you will receive credit for teaching and/or creating an IBBA course or workshop? For participating on a conference panel? You will receive credit for serving on a committee, being a chairperson or member of the board of directors. You can also submit completed transaction forms and will receive 10 credits for each transaction.

The IBBA even recognizes some non-IBBA courses. If you’ve completed an accredited course, 4 or more hours in length and have a valid course completion certificate you may be eligible for additional recertification credits.

Forms and additional information are available at IBBA.org. If you have questions, feel free to contact me or the IBBA staff.

Happy Recertifications!

Jeff Snell, IBBA Credentialing Committee Chair

IBBA Mid-Year Report Webinar

Are you interested in learning more about what the IBBA has in store for the future and how the association is performing this year?

Join IBBA Chair, Scott Bushkie and, Executive Director, Kylene Golubski, as they review and discuss the IBBA’s strategic vision, goals and performance. Learn how far we’ve come AND what lies ahead!

We welcome all those in the profession to attend ad learn where the IBBA is going in the year ahead, and beyond!

IBBA University Announcement

The IBBA is pleased to announce the release of four new online courses and new lower pricing for both online course at ibbauniversity.org and live courses. New online courses include #150 – Building a Listing Inventory, #158 – Managing Transactions, #206 Managing the Due Diligence Process, and #208 – Managing the Closing and Orderly Turnover Process.

All new online courses and existing online courses can be purchased at ibbauniversity.org.

CONGRATULATIONS TO OUR 34 NEW CERTIFIED BUSINESS INTERMEDIARIES

The IBBA is pleased to announce that 34 members of the IBBA completed the required course work and passed the required exam at the IBBA 2016 Spring Conference in Orlando, Florida last month.

David Abbott

Jose Miguel Arreaza

Jennifer Bailey

Scott Balfour

David Britton

Joseph Caffrey

Ryan Cave

Thomas Chang

Raymond Copell

Paul Corrigan

Michael Davidson

Dave DeCamella

William Decanio

Nate Ernest-Jones

Martin Fishman

John Geiwitz

Mylo Gonzalez

Kyle Griffith

Carol Haefner

Andrew Holtgrewe

Rubeel Khan

Bob Leone

Audrey Lero

Eddie Lim

Vincenzo LoCricchio, Jr.

Dan Maloney

Michael Mangan

Bret McGowne

Robert Miner

James Neumann

Dru Pio

Don Pippin

Muhammad ALAM Qureshi

Jason Tuzinkewich

[/columns-container]

Apples To Apples? The Benefits (and Pitfalls) of the Market Approach

When used correctly, the Market Approach can be the most accurate method in determining a business’s value. This approach can take on many forms with most popular being the Direct Market Data Method (privately held comparable sales) and the Guideline Publicly Held Data Method (public company data). Some could even argue the income approach is a form the Market Approach since a cap rate usually begins with an average “rate” based on an average expected rate of return. In any case, we’ll explore the benefits and pitfalls of using this approach.

When used correctly, the Market Approach can be the most accurate method in determining a business’s value. This approach can take on many forms with most popular being the Direct Market Data Method (privately held comparable sales) and the Guideline Publicly Held Data Method (public company data). Some could even argue the income approach is a form the Market Approach since a cap rate usually begins with an average “rate” based on an average expected rate of return. In any case, we’ll explore the benefits and pitfalls of using this approach.

Guideline Public Company Data. In my opinion, this is one of the most overused methods of valuation, more specifically for smaller businesses (less than $20 million in sales). In the 2016 Duff & Phelps Risk Premium Report (Exhibit A-7 & A-8), the smallest category for publicly held company information (Guideline Portfolio 25) showed an average of $130 million in sales and 302 employees. My assumption is that no one could argue that a $100 million company would ultimately compare to a $1 million company…. other than possibly being in the same industry, there is little to no comparison from an investor standpoint.

Direct Market Data Method (DMDM). On the other hand, the DMDM approach is not used enough in my opinion. Why? For litigation purposes (divorce, partner dispute, tax), maybe it’s because there are too many variables to defend or “unknowns” in the comparable transactions. However, with as much information out there on actual private company transactions, I believe there is enough data to support a definitive market for just about every industry. Even if the transactions are not “exact”, as long as it’s in the same sub-industry and has similar performance characteristics, most would argue the calculated “price multiples” can be relied upon for a 100% controlling value.

Pitfalls of DMDM Approach. As mentioned above, arguably the most contested aspect of the market approach is how “comparable” the data actually is. Here are a few of the obstacles in choosing comparable transactions and how to navigate around them:

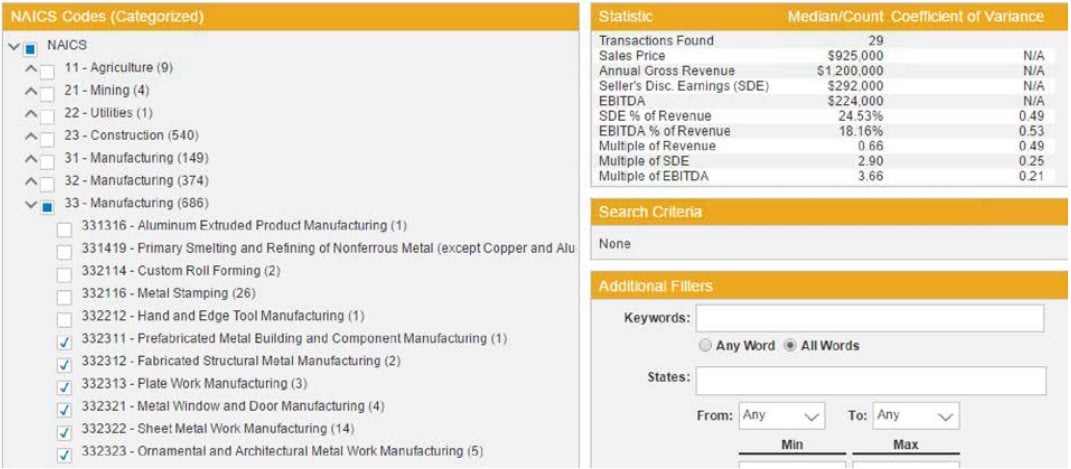

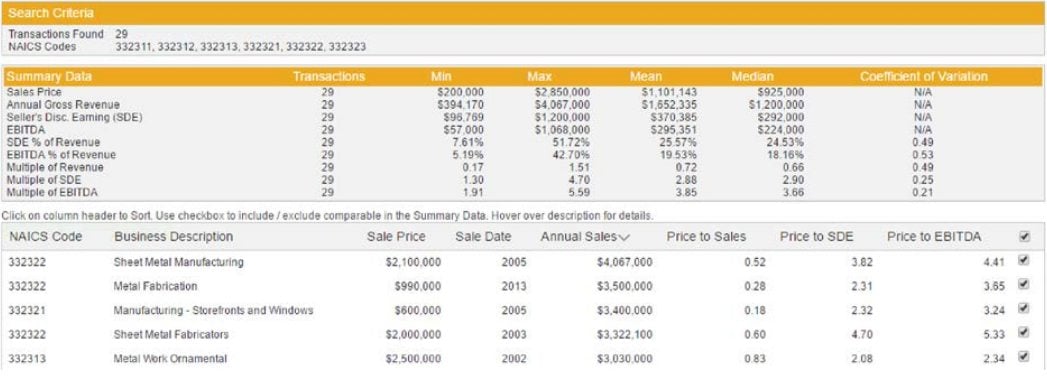

- Industry – you may or may not find the exact industry. If not, find the best sub-industry…. for example, the data sample below shows only 1 comparable transaction for “Prefab Metal Building and Component Manufacturing (NAICS 332311)”. I would suggest first expanding to the sub-segment, say NACIS 332300’s, which now shows a total of 29 comps. We now have enough comps to stratify into quartiles if we want.

Sample Data – Search Results for NAICS Codes 332311 thru 3332323

- Size – there is no exact science to choosing comps based on size. We tend to simply ask ourselves “what is reasonable”? It also depends upon how many comps you have to start with. If you are filtering “restaurants”, you can probably get away with a much tighter range (say all comps between $500,000 and $1 million in revenue. For our example above, we only have 29 comps so filtering based on size is not an option.

- Region – if you have enough comparable transactions, say restaurants, I would do a quick search based on state characteristics. For instance, the data sample below shows us that Liquor Stores in the state of New York sell for 20% higher than the state of California. Again, in our example, however, stratifying by region is not an option.

Sample Data – Liquor Store in New York

Sample Data – Liquor Store in California

- Performance Variables – most comp databases (including the data shown) use some type of “Price to” ratio. This is calculated as purchase price divided by, say “SDE” (seller’s discretionary earnings). What SDE was used to arrive at P/SDE…. last year, average of last 3 years, trailing 12 months? What year SDE should you apply it to? The best answer can only be use your best judgement. Some databases may tell you and others will not. The database used for this example is typically based on a “most reasonable projection going forward”.

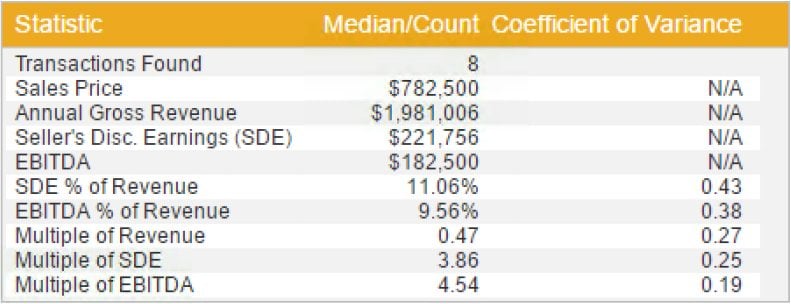

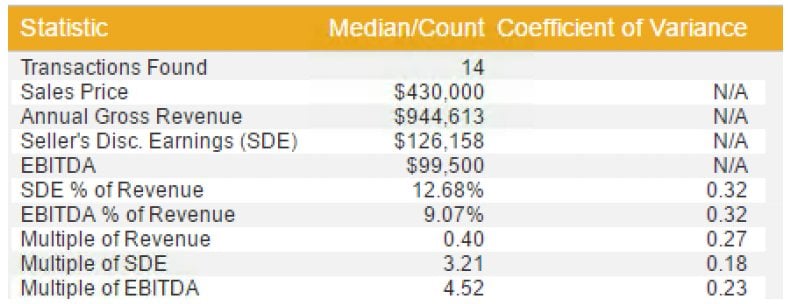

- Stratifying Price Multiples – once you feel comfortable with the transactions you’ve chosen, what “multiple” should you use…. average, median, highest, etc.? Without getting too technical, the lower the coefficient of variance the lower the volatility (more reliable). We typically look for a coefficient of variance lower than 1 and hopefully closer to .5. Other factors come into play as well…. size, performance trends, and overall “marketability factors”. In the below example, we’ve filtered our comps based on revenue size. As you see below, the top 5 price to SDE comps (based on revenue size) average to be 10% higher vs the 5 lowest revenue transactions. This could tell us that if our subject Company is generating say $3 million in revenue, maybe we should use a price to SDE multiple above the median (say top 25%).

Sample Data – Top 5 comps based on highest revenue

Sample Data – Top 5 comps based on lowest revenue

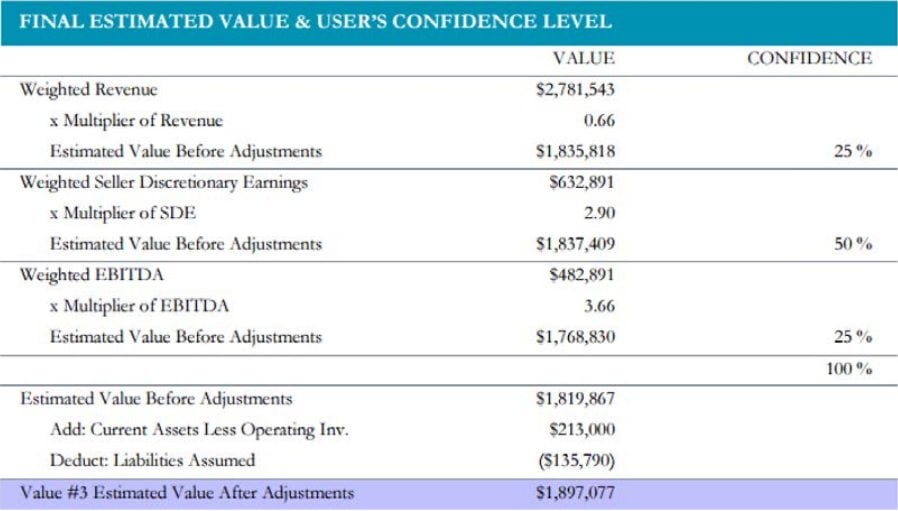

- Price and Value allocation – the biggest question we get at our firm is, “what does the value include” (and more specifically, inventory)? It’s well known that multiples in BizComps don’t include inventory; however, all other databases including our sample database, include inventory in the “price multiples”. Most databases also exclude cash, A/R, real estate and liabilities. Therefore, your final value calculations will look something like this:

Sample Data – Final Estimated Values

*current assets less operating inventory includes cash, A/R, and other current assets. ** all sample data in this article was obtained using PeerComps.com

*current assets less operating inventory includes cash, A/R, and other current assets. ** all sample data in this article was obtained using PeerComps.com

The market approach (DMDM specifically) is not perfect; however, it is the only small business valuation method that takes into consideration an “apples to apples” comparison. It is easily calculated and easy to explain to a client, lender, or the court. If you have access to the right data and use it correctly, it can be a valuable tool for business appraisers and business brokers.

Steven A. Mize, is the Managing Partner at GCF Valuation, Inc. and PeerComps, Inc. Steve is an accredited Senior Appraiser with an extensive background in the business valuation. Please feel free to contact him at [email protected] with questions on this article or with any other business valuation questions.

EMAIL YOUR SENATOR TODAY

Dear Members,

We need your help regarding the pending legislation in the Senate today! If this doesn’t pass, it could cost you tens of thousands of dollars one day!

Why? It is still against the law to transfer the ownership of a business using securities (i.e. stock sale and or perhaps even the use of a promissory note in an asset sale).

What Have We Accomplished To Date?

- Three SEC no Action Letters that help protect you, BUT IT DID NOT CHANGE THE LAW!

- Several states are considering adopting new regulations to match the No Action Letters

- HR 1765 (an omnibus bill) has been passed by the US House of Representatives.

- S. 1010 a bill with some restrictions, currently in the Senate and if passed would change our industry forever!

We’ve Come A Long Way Brokers…But you must take action NOW!!! If we miss this opportunity, it will take us at least another year or two to get to this crucial point.

Then get 10 people you know to do the same thing!!!

We also need companion legislation in most States! Want to help in your home State? Contact us now!

Click on the following links to learn more:

For more detailed information or to download a Pledge Card to support the effort, please visit our Legal Updates page.

Please contact John Johnson or Linda Purcell to find out how you can help.

Co-Chairs, Strategic Issues Task Force;

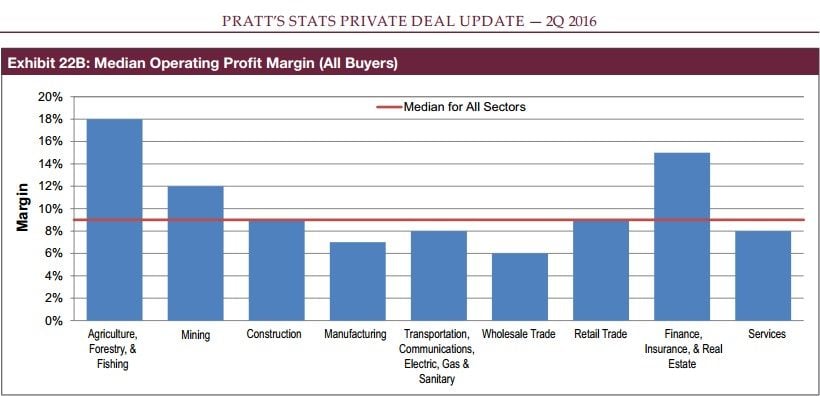

The information provided below is excerpted from the Pratt’s Stats Private Deal Update: 2nd Quarter 2016, which is copyrighted by and available exclusively from Business Valuation Resources, LLC. Brokers who contribute transaction details to Pratt’s Stats on closed business sales receive the complete Private Deal Update plus three months of free access to the database for each deal included in Pratt’s Stats.

The quarterly Pratt’s Stats Private Deal Update (PDU) provides general trend information on valuation multiples and profit margins for transactions in the Pratt’s Stats database, available exclusively through Business Valuation Resources, LLC (BVR) at www.BVMarketData.com.

Financial advisors, merger and acquisition professionals, business appraisers, business brokers, investment bankers and many others use the Pratt’s Stats database to determine the value of their subject company by applying the market approach with comparable company data.

Pratt’s Stats is the premier source for private business purchase details and includes both private and public buyers with over 140 data points that highlight the financial and transactional details of the business sales. As of the publication date, the Pratt’s Stats database contains 17,731 transactions in which the buyer was a private party. The database includes over 24,818 transactions in which a privately held company was sold to either a private or public buyer.

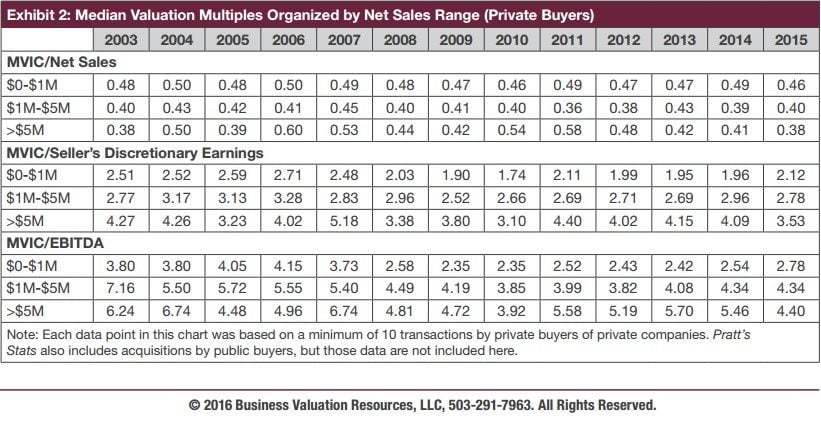

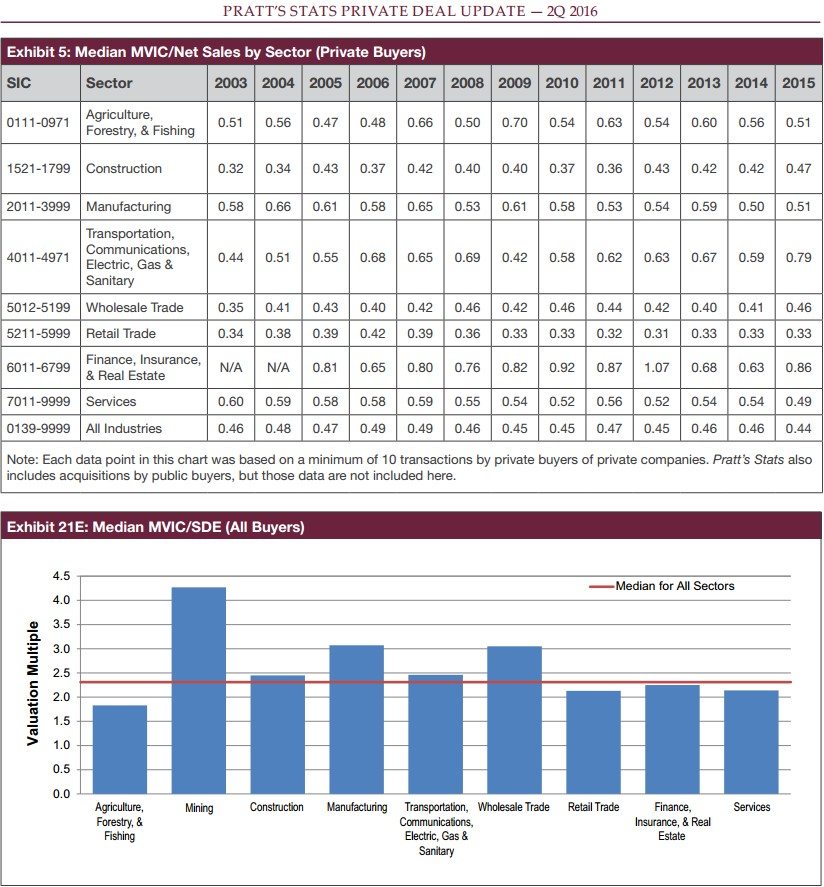

The charts and graphs presented below display median values.

MVIC: Total consideration paid to the seller and includes any cash, notes and/or securities that were used as a form of payment plus any interest-bearing liabilities assumed by the buyer. The MVIC price includes the non-compete value and the assumption of interest-bearing liabilities and excludes (1) the real estate value and (2) any earn-outs (because they have not yet been earned, and they may not be earned) and (3) the employment/consulting agreement values.

International Business Brokers Association

Members who submit completed transaction information receive a three-month complimentary subscription to Pratt’s Stats, for each included deal, as well as a complimentary subscription to Pratt’s Stats Private Deal Update, a quarterly publication analyzing private company acquisitions from the Pratt’s Stats database. Pratt’s Stats collects private business transactions of main street businesses from business brokers, as well as from middle market M&A advisors where a public company purchases a private company. The Pratt’s Stats database is updated monthly with an average of 100 transactions. Pratt’s Stats users enjoy:

- Easy searching that identifies comparable transactions by keyword, revenue range, industry name, SIC code, profitability margins, company name, and more

- Hard-to-find data on how deals are structured including payment terms, purchase price allocations, employment agreements, non-compete agreements, private company financial statements, private company financial ratios

- Valuation multiples that point to the greatest value drivers

-

- The ability to track market pricing trends via Pratt’s Stats timely deal updates

- Access to payment term information including contingency payment and transaction fee details

- Asking price vs. selling price comparisons for spread analysis

- Listing date and selling date inclusions for timeon-market analysis

For more information about Pratt’s Stats, contact Doug Twitchell at [email protected], Adam Manson at [email protected], or Mitchell Cameron at [email protected] or visit www.BVResources.com/ Contribute to learn more.

Pratt’s Stats – Financial Details on 24,815+ Business Sales

As a key stakeholder in the transfers of private businesses, you know how crucial comparable business data is to pricing your clients’ companies. Pratt’s Stats, published by Business Valuation Resources (BVR) and featured in Inc. Magazine and the New York Times, contains detailed financial information on 24,815+ acquired private companies.

BVR invites you to submit your closed transaction details to Pratt’s Stats, the leading private company transaction database. In exchange you’ll receive complimentary access to: 1) all financial and transaction data in the Pratt’s Stats database, 2) a subscription to the Pratt’s Stats Private Deal Update™, and 3) use of the new, time-saving tool, Pratt’s Stats Analyzer™. You can submit confidentially—we won’t disclose any information you do not wish to.

3 Easy Steps to Submit

- Register online at: bvmarketdata.com/contribute

- Gather your closed transaction deals and login

- Click on “Submit Deal” and complete the form (you can also submit closed transactions via fax/email). If you have a larger quantity of closed transactions to submit (100+), a BVR representative will travel to your office (free of charge) to review and enter the deals!

Submit Your Closed Transaction Details and We’ll Give You:

- 3 months of FREE access to Pratt’s Stats for EACH closed transaction you submit that’s included in Pratt’s Stats

- Pratt’s Stats Private Deal Update – a quarterly analysis of private company acquisitions by private buyers from the Pratt’s Stats database

- Use of the Pratt’s Stats Analyzer – a time saving tool to help you more easily and quickly analyze the sales you find in your searches

- Listing in BVR’s referral directory – used by sellers and buyers searching for intermediaries

- Chance to win an iPad Mini for EACH closed transaction you submit that’s included in Pratt’s Stats. The more sold deals you submit, the more entries you receive into our quarterly drawing.

Don’t wait – submit your transactions today and reap the rewards!

For more information, please contact:

Mitchell Cameron or (971) 200-4837

How Much Is A Business Worth? Does The Answer Fit In A Book?

Yiannis Empeoglou, CBI®, member of the IBBA since 2005, has completed translating the Greek original he published in 2012, so it is no longer “all Greek to you”! Plus, you have the chance to buy the book with a 25% discount!

Yiannis Empeoglou, CBI®, member of the IBBA since 2005, has completed translating the Greek original he published in 2012, so it is no longer “all Greek to you”! Plus, you have the chance to buy the book with a 25% discount!

No, you don’t have to worry. This is not avaluation textbook. Nor is it anything like these compulsory recasting and pricing courses that everyone dreads and fears before actually completing the CBI® exam and realizing that it was not that bad after all.

The book presents in plain English and in a manner accessible and understandable to everyone a complete and scientific response to perhaps the most difficult question in the world of small and medium businesses.

The book will equally benefit the business owner who reall does not have a clue about the value of his business, the semi-ignorant business owner who heard from an “expert” that his business is worth X times earnings and the professional business broker intermediary who has to deal with them all. Even if you are a seasoned pro and pricing a business appears trivial to you (trust me it never is), the book will help you answer all the usual objections Sellers have in order to justify the one and only, universal and truly infallible valuation method: “this is how much I want”.

Have you ever heard the phrase “my business has great potential” or “there is plenty of unreported cash, buyers will understand when they see the business” or how about “all I am asking for is what I put in the business, I am not asking for Goodwill”? Well, guess what, you are in good company.

The book is full of real examples and data from the world of small and medium businesses. Yes, full of Greek examples,but explanatory boxes for the benefit of the international reader have been added wherever necessary.

What else is in it for you? A thorough exposition of the philosophy behind the numbers, a small (but simple) plunge into Finance theory, a detailed explanation of why “all Profit is NOT created equal” and how to correctly use multiples, how synergies affect the value of a business and of course real world data and examples, including a demystifying section for the infamous DCF method.

The book has enjoyed considerable success in Greece. I have presented numerous seminars based on the book to business owners, employer associations like the Federation of Industries of Northern Greece (FING) (www.sbbe.gr) and trade associations like the European Language Industry Association (www.elia-association.org).

Even if you do not feel like reading another book on business value, allow me to suggest that you give the book to your clients, or prospective clients. Even better, give it to your Greek-American clients.

I secured one of my best assignments because a young lady decided to buy the book as a gift to her father who was approaching retirement age. At a price of € 30 ($ 33 with the discount you get) the book is a great door opener. Ialways have one on my desk when I speak to a prospective client.

You will find more information on my book on https://howmuchisabusinessworth.wordpress.com/. The book is available through Amazon (all the Amazon websites). Here is the link to my book on the .com site: https://www.amazon.com/much-business-worth-YiannisEmpeoglou/dp/1511862947/ To get the 25% discount you have to go to https://www.createspace.com/. Createspace is an Amazon company but unfortunately does not allow me to offer discounts through the Amazon websites. If you lose this link and go to the CreateSpace home page, right next to the Login and Sign Up buttons there is a little arrow next to the word “Site”. Click the arrow, pick “Store” from the drop-down menu and then proceed to shop for the book. You will need to create an account with CreateSpace.

Your discount code for a 25% is DK7YSUEZ. The discount is valid till August 31st, 2016. I am even throwing in an extra 10% discount, but it comes at a price! You have to agree to write a review on my book on Amazon. Send me an e-mail through the IBBA website and I will give you the code for a 35% discount.

I will more than welcome your comments on my website. Have fun reading! I hope that by the time you finish reading the book you will agree with me that it takes a book to answer the title question and that although there may not be a single correct answer, there are definitely many wrong answers. And these wrong answers have the nasty habit of getting into our clients heads.

Yiannis Empeoglou

New Member Section

Welcome to our new Members of the IBBA family!

Edward Adams

Christopher Andrews

Jack Armstrong

David Ball

Antonio Bardy

Jeffrey Baxter

Erin Bean

Jack Beraha

Rupesh Bharad

Anil Bhatia

Stephen Blain

Robert Bourgeois

George Bradbury

Brad Breckenridge

Joseph Caffrey

Alan Carter

MJ Cassner

Ryan Cave

Warren Cave

Gerard Chadwick

Aniss Cherkoui

John Clausen

Aaron Comeaux

Tom Conroy

Kate Constantakis

Justin Cooke

Raymond Copell

Paul Corrigan

Servando Cortez

Lidia Couzo

Max Crescenzi

Brian Cross

Jeff Cushing

Thandron Dadaille

Robert Daudt

Carey Davis

Erik De Renouard

Robert Dean

Dave DeCamella

Steven Denny

Benjamin Dobkin

Debbie Dolan

Frank Dolan

Michael Drury

Bob Dunphy

Randi Edwards

Dan Elliott

Scott Evert

Richard Fewell

Jessica Fialkovich

Albert Fialkovich

Terri Fletcher

Tom Flowers

Ron Garrett

Vikki Garrett

John Geiwitz

Ralph Geronimo

Thomas Gesimondo

Joseph Goldberg

Fatima Grady

Karl Grasemann

Jason Grindall

Justin Grolley

Ernest Grooms

Mustafa Gurleroglu

Erik Haas

Charles Harvey

Frank Havercamp

Sharon Heaton

Randy Hendershot

Joe Hige

Scott Hislop

Phil Holt

Bob Holt

Bob Hough

Mike Hoyle

Roger Hutson

Jay Inbar

Patricia Jennex

Laurel Johnson

Carolyn Johnson

Cristiana Jones

Mike Keen

Rich Kelm

Alex Keylikhes

Rhett Kniep

Brian Knoderer

Fred Koenig

Ed Krajcir

Pannkaj Kummar

Ellie Kwak

James Lascano

Robert Latham

Cal Lawson

John Lichter

Malcom Lilly

Mike Limbers

Dan Long

May Lu

Tom Macatee

Heather Madland

Shannon Madrid

Enrique Marchese

Garvin Mark

Greg Marquez

Dana Marsden

Marie Marsden

Cecil Martin

Phil Mason

Scott McKee

Lex Meredith

Robert Mitchell

Pooya Mohit

James Neumann

Vinh Nguyen

Lieu Nguyen

Lieu Nguyen

Michael Nolan

Wyn Norris

John O’Connor

James O’Sullivan

Lee Panitz

Rick Parker

Satish Patel

Daniel Pendersen

Scott Phillips

Fred Philips

Kevin Pickolick

Pamela Piper

Megan Powell

Domenic Rinaldi

Brad Roberson

Jon Roman

Art Rosenberg

Antonio Ross

Larry Sage

Paul Sartin

Michael Shea

Chris Smith

Don Smith

H. Joe Strickland

Gary Soloway

Tiffany Swartz

Alicia Taylor

Jared Thompson

R. Stephen Thomson

Stan Van Etten

Lisa Veltri

Mike Veltri

Bill Verret

Bryan Vescio

Douglas Walker

Art Warsoff

William Wicht

Jan Wild

John Winterburn

Scott Withers

Ray Wurth

David Yezbak

Joan Young

Mike Zarinbaksh

JUST ANNOUNCED MEMBER BENEFITS

IBBA MEMBERS NOW

RECEIVE FREE ACCESS TO PEERCOMPS & THE BUSINESS

REFERENCE GUIDE – A $799 VALUE!

Not A Member? Join Now To Save!

Upcoming Educational Summit

The 2016 Fall Educational Summit will be held in Cleveland, Ohio August 21 – 24 and will offer courses #210, #220, and #221. Registration will open, and additional details will be released at a later date.

IBBA Magazine

IBBA Magazine