home » News » Main Street News December 2015 – 4th Quarter

A Message From The Chair

Dear Members and Colleagues,

As another year draws to an end, it is important to reflect on all we have experienced throughout the year. I am thankful to have had so many IBBA experiences with you. I would like to wish everyone a Merry Christmas, Happy Holidays and a Blessed and prosperous New Year.

All the best, Cress V. Diglio

Chair of the Board

2015 IBBA Fall Conference – Albuquerque, New Mexico

Here are just a few of our favorite Conference pictures! Speed Funding was a hit; workshops were packed; and mastermind sessions were robust. Congratulations to our award winners and thank you to our sponsors and exhibitors! See you in Orlando, Florida May 2-7th for the 2016 IBBA Spring Conference!

Jeff Snell, CBI, M&AMI – November, 2015

When Not to Hire a Business Broker

Many words have been written about why you should hire a business broker (including by me) but when I searched online for why not to hire a business broker every article on the first several pages (save one that I wrote in 2011 and had forgotten about) was why a business owner should hire a business broker or questions to ask one before hiring one.

In this article I explore some of the reasons a business owner should go it alone and not retain a business broker.

Answer these questions and keep a tally of your answers.

Is the business more than about two years old?

Can the business run effectively for an extended period without you?

Do you have accurate up to date financials?

Have you reported all income to State and Federal agencies?

Is the majority of your business spread among many customers?

Does the business generate more than $50,000 of annual net profit?

Is it hard to start a similar business (expense/time/skills)?

Have the sales been stable or gradually increasing?

Would you describe your employees as loyal and committed?

Are you able to easily make payroll?

Would you buy this business knowing what you know about it?

If you recorded more than 2-3 “no” answers you may want to consider foregoing a business broker. If you answered “no” to either of the last two you may need to consider attempting to sell at all. Too many “no” answers and the broker, no matter how experienced, doesn’t likely have enough to work with to effect a successful transaction at a price that can be justified.

So, if hiring a broker isn’t the right course, then what is?

My advice would be to have a business valuation completed so that you have a clear idea what the fair market value of the business, related assets, and inventory are worth. Cost from $1,000 up. My firm charges $2,500.

Market the business as a FSBO (for sale by owner). The most effective way to do this in my opinion is to get an account at www.bizbuysell.com and complete the listing template. You will get a lot of exposure at a reasonable price without having to monitor and maintain a dozen or more listing sites like most brokerage firms manage.

When you receive buyer prospect inquiries understand that most have not ever owned a business, much less purchased a business. Step one should be financially qualifying the prospect. If they don’t have the money required for a down- payment it’s a waste of everyone’s time. Ideally they can get a prequalification letter from an SBA lender. It’s also usually critical that they already live near the business. The fact is people very rarely move to purchase a small business.

Be prepared to provide profit and loss statements, balance sheets, tax returns, an asset list, and any information about inventory. Be prepared to talk about why you are selling, operations, cash flow, customers and vendors.

If the business has issues disclose them early in the conversation – they will be discovered and better that you raise them.

Require that the buyer have a transaction attorney (not just “an” attorney) draft the letter of intent and the definitive purchase agreement. Have a transaction attorney review on your behalf. Don’t get cheap here. Insuring that what has been agreed to is what has been papered is extremely important. Remember it’s not what you get, it’s what you get to keep. You and the buyer are the decision makers. The attorneys are present to provide legal counsel so that YOU can make informed choices.

Any Seller or Owner financing should be personally guaranteed by the buyer and their spouse. The Sellers attorney should additionally file a UCC for the business assets being transferred.

There are many moving parts in any business transaction. If you feel that the process becomes overwhelming or that it is consuming too much of your time consider retaining an advisor that is willing to work for a reasonable hourly or up front flat fee. As they say “The thrill of low price is quickly forgotten when the reality of poor quality is realized.

Jeff Snell, M&AMI, CBI, ABI is the founder and Principal Broker of ENLIGN Business Brokers, a member of the International Business Brokers Association [IBBA] where he services as the Credentialing Chairman and a member of the Merger & Acquisition Source [MAS] where he service on the Credentialing Committee. He is also accredited by the American Business Brokers Association as an Accredited Business Intermediary [ABI].

Michael Fekkes, CBI – November, 2015

Benefits of Structuring Small Business Transactions

Michael Fekkes is a Senior Broker at Enlign Business Brokers in Nashville, TN. Michael is a Certified Business Intermediary [CBI], a member of the International Business Brokers Association [IBBA], as well as a former business owner.

Selling a privately held business is often romanticized as face-to-face negotiations over business valuations and purchase price. Whether small or large, these transactions can be extremely complex and require a great deal of work behind the scenes. As the size and/or complexity of a transaction increases, the need for innovative structuring options also increases. Deal structure, financing, and tax management must be a proactive process that is addressed at an early stage. In many cases the Seller and Buyer often place all of the focus on the transaction price at the expense of the ‘net results’ of a business transaction. By carefully negotiating the terms and structure of the transaction, a business seller could walk away with a deal that provides a significantly larger economic benefit than a transaction that provides 100% of the proceeds at closing. For asset sale transactions, the ‘allocation of purchase price’ can become another area of negotiation after the price, terms and conditions of the sale have been agreed to by the buyer and seller.

Each type of structure carries with it different tax consequences for the buyer and seller, having a material impact on the overall value of the transaction. The type of business entity owned by the seller (C-corporation, S- Corporation, LLC, Partnership, or Sole Proprietorship) in addition to whether the transaction becomes an asset sale or stock sale will have a major bearing on the decisions made in structuring the transaction to afford maximum economic benefits.

The purpose of this communication is to advance a few of the techniques available in structuring small business sale transactions and to emphasize the value an experienced team brings in structuring the transaction. Asset sales of pass-through entities (LLC, S-Corp, & Partnerships) are handled very differently than stock-sales of C-Corps and it would be impossible to cover all of the structuring alternatives within this short document. Proper legal and tax counsel should be retained and the cost of these professionals is usually offset by the benefits they bring through their involvement in the transaction.

The following factors will be relevant in structuring the transaction:

1. Legal Business Entity

a. LLC

b. S-Corp

c. C-Corp

d. Partnership

e. Sole Proprietorship

2. Type of Sale

a. Asset Sale

b. Stock Sale

3. What is being sold

a. Entire business

b. Partial Interest / Investment

c. Inclusion of Real Estate

4. Installment Sale or component of Seller Financing

5. Who is the buyer

a. Financial Buyer (Entrepreneur)

b. Strategic Buyer:

i. Corporation

ii. Private Equity Group (PEG)

c. Family Member (Succession)

6. Plans after the sale (Short term/Intermediate/Long Term)

a. Consulting Contract

b. Employee Contract

c. Covenant not to Compete

7. Personal Tax Situation

Asset Sale/Stock Sale

Determining what is being sold, the individual assets of a business or the stock in a corporation, will be critical in determining the optimal structure of a transaction. The majority of small businesses that are sold each year are structured as an asset sale. An asset sale is when a buyer purchases all or a portion of the assets of a business (e.g., facilities, equipment, vehicles, real estate, etc) whereas a stock purchase is the purchase of the ownership shares/rights of the corporation – all assets and all liabilities of the entity are retained by the corporation and only a change in corporate ownership has occurred. The following highlights three notable differences between each method; there are many additional considerations so it is critical to consult professional advice to determine the most appropriate method.

Change in Legal/Tax Entity:

With an asset sale, the legal entity and tax identity do not transfer to the purchaser. The Buyer receives a stepped-up tax basis in the assets acquired equal to the FMV purchase price, the point from which new depreciation is started. Under a stock sale, the tax basis of the assets remains unchanged, and all of the tax attributes, including depreciation methods, tax year, corporate tax election, are preserved.

Liability

With an asset sale, the Buyer’s liability is limited. The Buyer is purchasing some or all of the assets and has the option to identify any liabilities they are interested in assuming. Under a stock sale, the Buyer purchases the stock of the company and assumes all liabilities (known, unknown, contingent or otherwise).

Assignment of Contracts

Most businesses have contracts in one form or another. The most common are commercial real estate leases, contracts involving business relationships, and contracts with employees. An asset sale transaction involving the assignment of these contracts requires considerably more work and has a potentially a different outcome than a stock sale. Contracts need to be evaluated to determine if they permit an assignment without consent. Should they not permit assignment without consent, third party consent will need to be obtained. In stock sale transactions, the legal entity that is the party to the contract continues, and the general rule is that the contract remains in force between the original parties. (No consent to assignment is needed as assignment typically does not occur). There are exceptions, as some contracts stipulate that a change in ownership of the business will be considered an assignment of the contract. If such a ‘change of control’ clause exists in the contract, the same issues will arise as with an asset transaction. Performing due diligence and having legal counsel thoroughly review all of the company’s contracts will be critical to determine the available options.

Covenant Not to Compete

A covenant not to compete (CNTC) is a contractual condition by which the seller promises to refrain from conducting business or professional activities of a nature similar to those of the business being sold. In a contract for the sale of a business, a reasonable value can be allocated to a ‘covenant not to compete’ which is generally enforceable provided it is reasonable and limited as to time and territory. The buyer may amortize this amount over 15 years even though the actual term of the CNTC is usually much shorter. For this reason, buyers often prefer a larger amount be allocated to tangible assets or a consulting agreement with a shorter useful life. In order to be legally binding, it is recommended that some consideration is allocated to a CNTC.

Consulting Agreement

Depending upon the goals of the seller/buyer and the complexity of the business being sold, the seller could be retained as an independent consultant. The consulting agreement should specify the schedule of time (days or hours involved), type of training or services provided, the length of the agreement, and compensation. This is a popular structuring method which can benefit both the buyer and seller. For example, the sales price could be lowered in exchange for a lucrative consulting contract. The buyer benefits as they pay less money up front and have the ability to deduct the payments in the year made as a business expense. The seller could benefit by receiving the compensation over a period of several years, possibly reducing the tax impact. There are additional tax related issues to the seller, pertaining to the deductibility of business expenses incurred as a consultant and potential self-employment taxes, and it is therefore recommended that proper tax counsel is obtained.

Seller Financing/Installment Sale

It is rare for a privately-held business to change hands for an all-cash price. More common in small business sales would be to have a component of seller financing as part of the deal structure. Seller financing is a mechanism where the business owner would fund the sale of their business and/or business assets with a promissory note helping the buyer finance all or a portion of the acquisition of the business and/or business assets, which is then paid back from the business’ cash flow. This type of deal can be very flexible — the seller can adjust the payment schedule, interest rate, loan period, or any other terms to reflect the seller’s needs, business cash flow, and the buyer’s financial situation. There are several benefits to the business owner in providing seller financing:

Maximization of Transaction Value

Few areas offer more opportunity to negotiate successfully than when it comes to the details of the financing. Many sellers actively prefer to do the financing themselves as they can negotiate the highest transaction value when offering flexible owner-finance terms. In addition, the interest earned on the promissory note will add significantly to the actual selling price. Interest rates are currently hovering at their lowest level in years and sellers recognize that they can get a much higher rate from a buyer than they can get from any financial institution.

Tax Benefits

Seller financing could be a way for the owner to defer tax on the sale of the business. If the sale complies with the IRS installment method of reporting for tax purposes, capital gain taxes could be recognized when payments on the seller financed note are received versus 100% of the gain recognized upon closing the sale. It will be important to consult a tax professional as not all assets would qualify for deferred capital gains treatment. Typically, the assets that have depreciated beyond their original purchase price, such as real estate, are eligible for installment sales, as are intangibles (such as goodwill) that are established during the course of the business.

Completing the Transaction

Seller financing can be a useful tool to complete business sale transactions that need extra financing as part of their structure. The pool of qualified buyers increases exponentially when a portion of the transaction is financed by the seller. For some businesses, carrying back a note for some or all of the purchase price may be the only way to sell the company. The credit market, as a result of the sub-prime financial crisis, is still very tight. The plentiful, easily obtainable, flexible and inexpensive credit that flooded the market several years ago has changed dramatically. Many buyers will leverage bank financing to acquire a business and the majority of these lenders will require a component of seller financing to underwrite the loan. Seller financing, in the lender’s eyes, mitigates risk as they will have the additional confidence knowing that the seller has a vested interest in the business succeeding. The seller, in this instance, will be providing secondary financing to the bank’s acquisition load (i.e. subordinated debt) for the remainder of the price.

In the event of a default by the buyer on the seller financing note, the seller would have a number of options for recourse and the specifics will vary per transaction based upon the involvement of a primary (1st position) lender, the extent of collateralized assets, in addition to personal guarantee’s made by the buyer. The specific rights will be detailed in the security agreement that is associated with the promissory note and can involve a number of stipulations including restricting the new owner’s sale of assets, acquisitions, and expansions until the note is paid off in addition to specifying the receipt of quarterly financial statements to enable the seller to keep tabs on the business. Having an experienced transaction attorney involved in the drafting of the promissory note will be essential.

Earn-Outs

An earn-out provision is an excellent structuring vehicle to bridge the gap on a valuation difference between what the seller expects to receive from a sale and what the buyer thinks a business is worth. Earn-outs are contractual contingent payments in which the purchase price is stated in terms of a minimum, but the seller will be entitled to additional compensation if the business reaches certain financial benchmarks in the future. Although the benchmarks can be calculated as a percentage of sales, gross profit, net profit or other figure, an earn-out is most often based on sales (not profits) and is typically tied to increasing revenue over historical levels. An earn-out is a good way to maximize the total selling price of the business, especially if the seller is confident of future sales and the new owner’s management ability. It is not uncommon to establish a floor or ceiling for the earn-out, and in a down economy, a seller can use an earn-out provision to obtain a value closer to what the business is worth in a healthy economic climate. Earn-outs are favorable to both the buyer and seller. The seller recognizes earn-outs as payment of money predicated on the future performance of the business and is therefore in a position to potentially obtain a higher value for their business than what would be afforded in a traditional sale in the current market. Buyers, on the other hand, are attracted to earn-outs as they pay less money at the time of sale but compensate the seller based upon the future success of the business. Buyers are protected against overpaying for a business that doesn’t meet the projections or growth that the original owners expected. Furthermore, Buyer’s recognize the vested interest the earn-out creates with the seller and the shared goal in the continued success of the enterprise. Most successful earn-outs are achieved when they are limited to one or two variables based upon a solid 3-5 year sales forecast. Earn-out provisions require a greater degree of involvement by the seller, and are most often implemented in conjunction with a seller employment or consulting agreement where the seller is positioned to ensure that all of the steps are being taken to reach the goals. Furthermore, it is also important to specify in the contract the person or firm that will be responsible for managing or reviewing the books and verifying the business’s performance.

Asset Allocation

In a small business sale, the owner is selling a collection of assets, some tangible (such as inventory, vehicles, buildings, and FF&E) and some intangible (such as software, customer lists, trade names, trained & assembled workforce, patents, non-compete agreements, and goodwill). Unless the entity is a C-Corp and stock is being sold, the total transaction price is allocated sequentially based on the fair market value of the acquired assets. The Tax Code shows that assets fall into 7 different categories (asset classes) based on IRC section 1060 (Form 8594), and requires that the buyer and seller adopt and maintain a consistent purchase price allocation method for tax future calculations that will determine both the buyer’s basis in the assets and the seller’s gain or loss. In most cases, the tax impact on the individual assets sold are measurably different for the buyer and seller and therefore the negotiation of the dollar amounts allocated to each of the 7 categories becomes an important element of the business transaction. Class I – Cash Class II – Marketable Securities Class III – Market to Market Assets & Accounts Receivable Class IV – Inventory Class V – Assets Not Otherwise Classified Class VI – Section 197 Intangibles other than Goodwill and Going Concern Class VII – Goodwill and Going Concern Value (Residual)

Minimizing taxes plays a major role in structuring and negotiating a business transaction. Many promising deals have fallen through because the buyer and seller couldn’t agree on how to structure the deal to minimize taxes. Typically, the seller seeks to have as much money as possible allocated to assets that would be taxed as capital gains versus assets that would be treated as ordinary income. The buyer on the other hand strives to have a larger weight allocated to assets that are currently deductible or where stepped-up assets could be depreciated quickly under IRS regulations. Particular attention should be paid to the identification and valuation of the “intangible” assets as they can be significant in negotiating terms. While Buyers are often indifferent to an allocation between goodwill and a CNTC, because Sec. 197 allows a buyer to amortize goodwill or a CNTC over the same 15-year period, they will often prefer a larger allocation to a consulting agreement which is able to be expensed in the year paid. Sellers, however, prefer goodwill & going concern allocations (capital gain treatment) over a CNTC or a Consulting Agreement (ordinary income treatment).

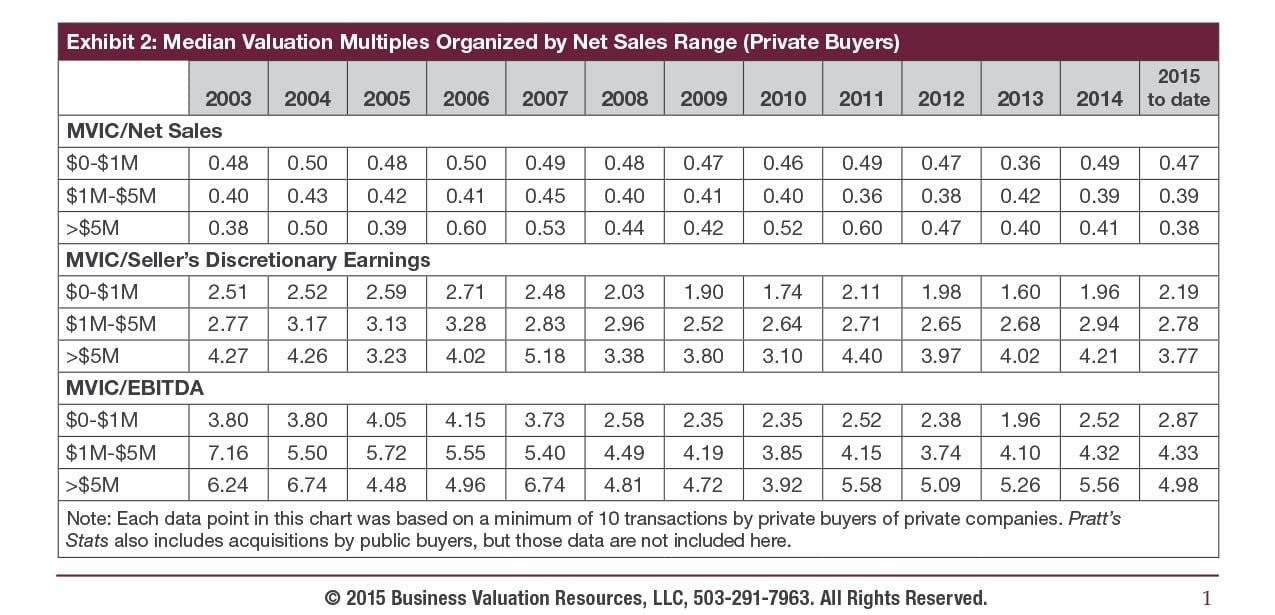

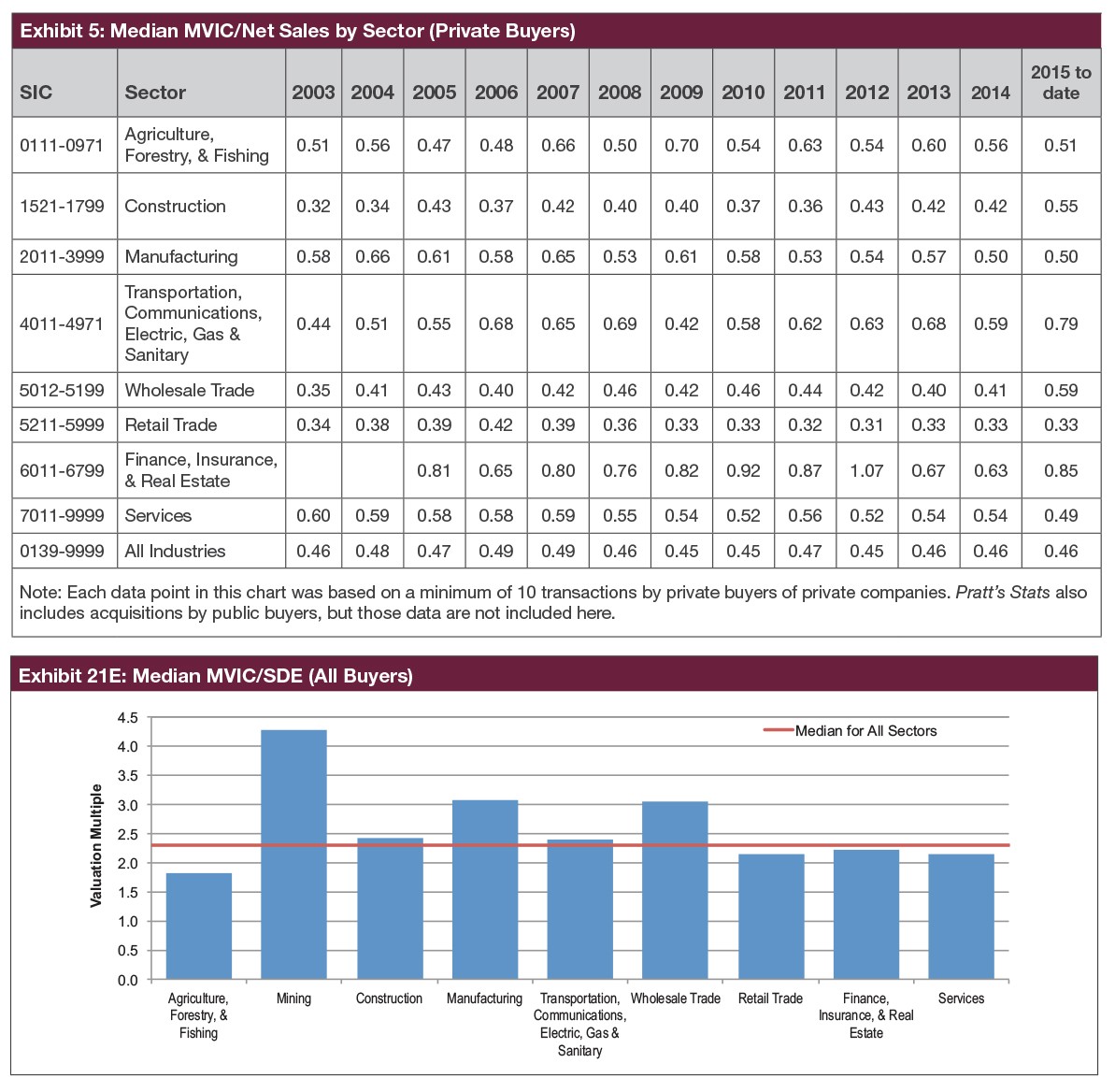

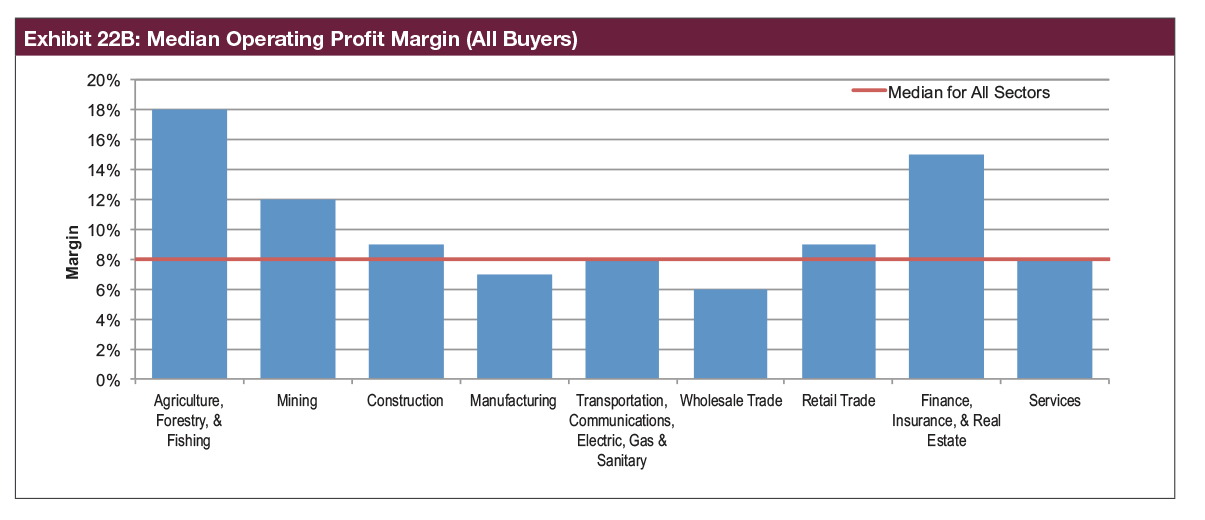

Pratt’s Stats Private Deal Update

The information provided below is excerpted from the Pratt’s Stats Private Deal Update: 4th Quarter 2015, which is copyrighted by and available exclusively from Business Valuation Resources, LLC. Brokers who contribute transaction details to Pratt’s Stats on closed business sales receive the complete Private Deal Update plus three months of free access to the database for each deal included in Pratt’s Stats.

The quarterly Pratt’s Stats Private Deal Update (PDU) provides general trend information on valuation multiples and profit margins for transactions in the Pratt’s Stats database, available exclusively through Business Valuation Resources, LLC (BVR) at www.BVMarketData.com.

Financial advisors, merger and acquisition professionals, business appraisers, business brokers, investment bankers and many others use the Pratt’s Stats database to determine the value of their subject company by applying the market approach with comparable company data.

Pratt’s Stats is the premier source for private business purchase details and includes both private and public buyers with over 100 data points that highlight the financial and transactional details of the business sales. As of the publication date, the Pratt’s Stats database contains 17,170 transactions in which the buyer was a private party. The database includes over 24,210 transactions in which a privately held company was sold to either a private or public buyer.

The charts and graphs presented below display median values.

MVIC: Total consideration paid to the seller and includes any cash, notes and/or securities that were used as a form of payment plus any interest-bearing liabilities assumed by the buyer. The MVIC price includes the non-compete value and the assumption of interest-bearing liabilities and excludes (1) the real estate value and (2) any earn-outs (because they have not yet been earned, and they may not be earned) and (3) the employment/consulting agreement values.

International Business Brokers Association – IBBA

Members who submit completed transaction information receive a three-month complimentary subscription to Pratt’s Stats, for each included deal, as well as a complimentary subscription to Pratt’s Stats Private Deal Update, a quarterly publication analyzing private company acquisitions from the Pratt’s Stats database. Pratt’s Stats collects private business transactions of main street businesses from business brokers, as well as from middle market M&A advisors where a public company purchases a private company. The Pratt’s Stats database is updated monthly with an average of 100 transactions. Pratt’s Stats users enjoy:

Easy searching that identifies comparable transactions by keyword, revenue range, industry name, SIC code, profitability margins, company name, and more

Hard-to-find data on how deals are structured including payment terms, purchase price allocations, employment agreements, non-compete agreements, private company financial statements, private company financial ratios

Valuation multiples that point to the greatest value drivers

The ability to track market pricing trends via Pratt’s Stats timely deal updates

Access to payment term information including contingency payment and transaction fee details

Asking price vs. selling price comparisons for spread analysis

Listing date and selling date inclusions for time- on-market analysis

Pratt’s Stats – Financial Details on 24,210+ Business Sales

As a key stakeholder in the transfers of private businesses, you know how crucial comparable business data is to pricing your clients’ companies. Pratt’s Stats, published by Business Valuation Resources (BVR) and featured in Inc. Magazine and the New York Times, contains detailed financial information on 24,210+ acquired private companies.

BVR invites you to submit your closed transaction details to Pratt’s Stats, the leading private company transaction database. In exchange you’ll receive complimentary access to: 1) all financial and transaction data in the Pratt’s Stats database, 2) a subscription to the Pratt’s Stats Private Deal UpdateTM, and 3) use of the new, time-saving tool, Pratt’s Stats AnalyzerTM. You can submit confidentially— we won’t disclose any information you do not wish to.

3. Click on “Submit Deal” and complete the form (you can also submit closed transactions via fax/email). If you have a larger quantity of closed transactions to submit (100+), a BVR representative will travel to your office (free of charge) to review and enter the deals!

Submit Your Closed Transaction Details and We’ll Give You

3 months of FREE access to Pratt’s Stats for EACH closed transaction you submit that’s included in Pratt’s Stats

Pratt’s Stats Private Deal Update – a quarterly analysis of private company acquisitions by private buyers from the Pratt’s Stats database

Use of the Pratt’s Stats Analyzer – a time saving tool to help you more easily and quickly analyze the sales you find in your searches

Listing in BVR’s referral directory – used by sellers and buyers searching for intermediaries

Chance to win an iPad Mini for EACH closed transaction you submit that’s included in Pratt’s Stats. The more sold deals you submit, the more entries you receive into our quarterly drawing.

Don’t wait – submit your transactions today and reap the rewards!

For more information, please contact: Zac Cartwright or (971) 200-4840

2014 Annual Report Now Available

Members can now download the 2014 Annual Report from the Member Center. The Report contains information about the financial performance of the association, as determined by an independent audit. The 2014 FYE audit was conducted later in 2015 than usual to reduce the cost of the audit. We will weigh the costs/benefits of delaying the audit again for the FYE 2015.

Marketing Your Business and Your Listings Online – Learning Webinar

December 9, 2015 – 12 p.m. EST

Learn about key drivers in today’s business-for-sale market, including how IBBA member transactions compare to non-IBBA members, as well as best practices for marketing yourself and your business online. Plus, gain an in-depth understanding of how to create stronger listings that get more exposure and generate more leads.

IN THIS ISSUE: “What Makes the IBBA Different” Letter from the 2026 IBBA Chair. Plus, Selling Businesses with Bad Financials, Navigating the Minefield of Restaurant Franchise M&A, and More!

Reflections on the 2026 Annual Conference and the Culture That Sets Our Profession Apart One of the privileges of serving as Chair is getting to see our conference from a different perspective. You see the energy in the room before the first session begins. You hear the feedback in the hallways. You meet first-time attendees […]

You have worked the deal for nine months. The seller is in Colorado, the buyer is a private equity group out of Chicago, and the deal is a stock purchase with a slice of rollover equity. Diligence is done, your success fee is papered, and your firm sits squarely inside the 2023 federal M&A broker […]

watch_later06/11/2026

Newsletter Sign UpGet the latest insights on buying and selling small businesses direct to your inbox.

If you recorded more than 2-3 “no” answers you may want to consider foregoing a business broker. If you answered “no” to either of the last two you may need to consider attempting to sell at all. Too many “no” answers and the broker, no matter how experienced, doesn’t likely have enough to work with to effect a successful transaction at a price that can be justified.

If you recorded more than 2-3 “no” answers you may want to consider foregoing a business broker. If you answered “no” to either of the last two you may need to consider attempting to sell at all. Too many “no” answers and the broker, no matter how experienced, doesn’t likely have enough to work with to effect a successful transaction at a price that can be justified.

IBBA Magazine

IBBA Magazine