Letter From The Chair

LOU VESCIO, IBBA CHAIR

Last year was a banner year for the IBBA and I want to personally thank Scott Bushkie, our 2016 Chair, and Kylene Golubski, our Executive Director, for their tremendous efforts to continue to make the IBBA a great association.

Last year was a banner year for the IBBA and I want to personally thank Scott Bushkie, our 2016 Chair, and Kylene Golubski, our Executive Director, for their tremendous efforts to continue to make the IBBA a great association.

I am often asked by members of our affiliates, “Why should I join the IBBA since I already belong to a business broker association in my state.” For those of us that are longtime members, it is an easy question to answer, the IBBA helps us to become Better Business Brokers so we can make More Money.

Of course, we must take advantage of our excellent educational courses, workshops, webinars, and benefits to become better business brokers. And by increasing our knowledge and skill sets by networking with fellow members from around the world, we are better prepared to handle the many complicated issues of selling a business. The result is greater Success and More Money!

I like to think of the IBBA as the educational partner to our many affiliate organizations. In 2016 we experimented with offering two Educational Summits to members of the Business Brokers of Florida, and the concept proved to be a great success. This year we have expanded our Educational Summit program to three different locations and have enrolled about 75 new students for the February and March offerings. Some of the affiliates are now asking us to bring more advanced courses to their meetings and local conferences and we expect to begin that activity this year. In addition, we continue to develop and update new online courses to make education even more convenient for our membership.

The IBBA 2017 Annual Conference is scheduled for May 5th through May 8th in Dallas, Texas. In addition to our course offerings, it will feature more than 20 new workshops and the ever-popular Mastermind Sessions, where members share their knowledge, experience and war stories. This Conference should be one of the best and largest in recent years and it is one you do not want to miss! Dallas and Fort Worth are great cities with many great restaurants, superb shopping, and tons of things to do, so plan to spend an extra day or two and enjoy the museums, professional sports venues, and legendary nightlife.

If you haven’t submitted your “done deals” for the IBBA Excellence Awards Program, please do soon. The IBBA Member Excellence Awards is a way to show your clients, referral sources and general public that you are a step above the competition and that this is just another reason why you are the best choice as their advisor! You can find all the information on the Awards Program by clicking here.

I would also like to thank the Board of Directors and all the committee chairs and volunteers. We accomplished a great deal last year, and we have bigger plans this year, and none of that is possible if not for our many members that selflessly volunteer their time.

Finally, if you have any suggestions on how to make the IBBA better, please call me at 321-255-1309 or email me at [email protected]. I appreciate those of who you have already reached out.

Continued success,

Lou Vescio, CBI, M&AMI, Fellow of the IBBA

Buyers Who Are Likely To Waste Your Time

JEFF SNELL, MICHAEL FEKKES; CBI, M&AMI

As a business transaction professional time management is a critical component to achieving success. Whether that is in qualifying potential buyers or selecting which business sellers to work with, the message is the same. There are only 24 hours in the day so the choices that are made as to where this precious time is spent and who are the beneficiaries will have a direct impact on the results a business intermediary is able to achieve.

As a business transaction professional time management is a critical component to achieving success. Whether that is in qualifying potential buyers or selecting which business sellers to work with, the message is the same. There are only 24 hours in the day so the choices that are made as to where this precious time is spent and who are the beneficiaries will have a direct impact on the results a business intermediary is able to achieve.

The goal of this article is to highlight a variety of situations that business intermediaries find themselves in that are typically red flags when working with buyers (dreamers, sneaky competitors, and professional tire kickers). We will address similar red flags for seller clients in our Q2 newsletter. Ultimately, it is up to the business intermediary to determine how much time they have available and whether they have the interest and fortitude to travel down some of these rabbit holes.

1. Financial Capability

There are several schools of thoughts as it relates to the registration or the preliminary qualification of a buyer prospect. Many firms choose a process to make it as easy as possible to solicit buyers with minimum requirements to demonstrate liquid cash and credit score to financially qualify. Some firms have a more comprehensive registration process requiring a PFS, bank statement(s) and detailed applications. Another approach is to use an SBA loan packager to prequalify a buyer’s financial wherewithal. All approaches can and do work. The bottom line is that buyers should be knowledgeable and prepared to disclose (or educated by broker) about the size of business they are qualified to purchase. Brokers who do not have the conversation at an early stage with the prospect to determine if they have the necessary funds (or ability to acquire them) to buy the listed business could be wasting time.

2. Being dishonest and lies of omission.

Buyer candidates who are dishonest, deceptive, or less than forthcoming with data necessary to properly evaluate them as a serious candidate should be disqualified from consideration. It is not appropriate for buyers to be cagey or evasive when working with a business broker. We require buyer candidates to be honest, direct, and forthcoming. If a prospect feels that they make the rules because they hold the checkbook it’s time to eliminate them. A prospect that is difficult at this stage will only get worse throughout the process.

3. Unrealistic Expectations

The list of unrealistic buyer expectations is long. Let’s start with those buyers who feel they are entitled to have access to customer, employee, or vendor names. In most cases this is just not appropriate prior to closing. There are many avenues to provide the necessary information needed to make a buying decision without divulging this highly sensitive data. Ask “what question are you trying to answer with this information?”.

4. Buyers who say “I am open to anything”

Most of these individuals are professional “want-trepreneurs”. They think they want to buy a business and be an entrepreneur but can never pull the trigger. How long have you been looking? -and- How many opportunities have you reviewed? Are you interested in a restaurant? How about an accounting firm? are good qualifying questions. Inquiring about multiple businesses at one time in completely different industries, markets and geographies is another red flag for this type of time waster.

5. Buyers who say “I have investors”

This is often fraught with peril. Understanding, from day one, who is the buyer of the business, who has the money, etc., will save a lot of time. In many cases, the cash flow available from the business for sale will support only one buyer so when multiple parties are involved, and the business is relatively small, it could be problematic. Understanding all likely players in the transaction, up front, will mitigate pain, and lost time, down the road. Have the “investors” sign the NDA and ask them directly how much they are willing to contribute towards a transaction.

6. Buyers who are unresponsive

Returning phone calls, emails, and demonstrating basic professional communication skills is important. Chasing prospects who are unresponsive to communications is rarely productive. Quick no’s are far better than slow no’s.

7. Buyers who seek 100% seller financing

We all get these calls, buyers looking for the seller to finance the purchase of their business. The idea of buying a business with little to no money down and financing the acquisition entirely out of the future cash flow of the business is not something that we would ever recommend. Yes, there are exceptions, but they are very rare.

8. Looking for perfect business with zero risk

Small business ownership involves accepting a reasonable level of risk. There is no such thing as a perfect business and those buyers seeking to eliminate 100% of risk typically are not ones who possess the mental fortitude to ever pull the trigger. I put these candidates in the dreamer category. In one conversation I asked the prospect how much he thought the seller should pay him to buy the business that was generating approximately $250,000 owner cash flow.

9. Buyers who overtly state that they are MBA’s

Having an educated (maybe even Ivy league) buyer at the table is great. BUT…it generally comes back to the IBBA basics. For main street businesses, we are generally looking at a multiple of SDE, not EBIT or EBITDA. Let’s not make this more complicated. With the majority of main street businesses, prospects are buying a job. Therefore, stay focused on owner benefit and do not get sidetracked with business school methodology, which in many cases, will only apply to middle market or public companies. MBA’s who want to change the focus to inappropriate methodologies, include excluded assets like cash on hand and accounts receivable are wasting everyone’s time.

10. Being Unprepared / Unwilling

Buyers should be able to convey, at the earliest opportunity, their investment criteria, time table, financial wherewithal and reasons for pursuing the acquisition. Why should a buyer expect to receive highly sensitive information from the Seller when they have not gone through the basic thought process to be viewed as a serious candidate?

11. Transferrable Skills / Licensure

While it is always preferred for buyers to have direct industry experience, the existence of transferrable skills also works. This skillset needs to have some relevance with the particular business they are seeking to acquire. If they do not have the skills or licenses to operate the business they need to look at other opportunities.

12. Ability to react quickly

An ideal buyer candidate is well organized, has done their research, and knows what they want and what they can afford. They are decisive and capable of moving through the process in a timely and methodical manner. They are prepared with a list of well thought and detailed questions designed with the objective of determining if the opportunity meets their investment criteria. Once the opportunity is qualified they are able to make a ‘realistic offer’ and provide, at a minimum, an IOI, LOI, or terms sheet and maintain momentum through closing.

As IBBA Members we should be exposing our listings to as many potential buyers as possible and be ready to respond, professionally, to every interested candidate. Having an understanding of the red flags and rabbit holes that could be time wasters, enables us to be more prepared to invest the lion share of our time with those candidates who demonstrate they are sincere, prepared, and financially capable to pull the trigger at the appropriate time. We need to be selective of the buyers we engage with to protect our client’s confidential business data. In facilitating this process we will invariably have to kiss a few frogs – just make sure they aren’t so long you fall in love.

In August of 2003 Mr. Snell formed ENLIGN Business Brokers and has since added ENLIGN Advisors specializing in lower middle market transactions and ENLIGN Commercial focused on commercial real estate transactions. He is a Merger & Acquisitions Master Intermediary, a Certified Business Intermediary and an Accredited Business Intermediary. He has been awarded the International Business Brokers Association Fellow of the IBBA award and currently serves on the Board of Directors and as the IBBA Credentialing Chairman. Over the past 27 years he has worked in various capacities in the technology industry, professional services, consulting as well as board level positions with several unrelated firms and associations. He serves on the credentialing and conference committees of the Merger & Acquisition Source and is active in his church and is recognized by the University of Chapel Hill Keenan-Flagler MBA school as a regular speaker, coach, mentor and judge in business plan competitions. He lives in Raleigh, NC with his wife Melissa of seventeen years and four young children. –ENLIGN Business Brokers is a Professional Services Firm serving the Southeast that is headquartered in Raleigh, NC providing business intermediary services ranging from valuation and sale to exit & succession planning strategies.

Michael Fekkes is a Senior Broker at ENLIGN Business Brokers in Nashville, TN. Michael is a Certified Business Intermediary [CBI], a Certified Exit Planning Advisor [CEPA], Chairman of the International Business Brokers Association [IBBA] – Communications Committee, as well as a former business owner. He can be reached at 910.691.2202 or [email protected]. –ENLIGN Business Brokers is a Professional Services Firm serving the Southeast that is headquartered in Raleigh, NC providing business intermediary services ranging from valuation and sale to exit & succession planning strategies.

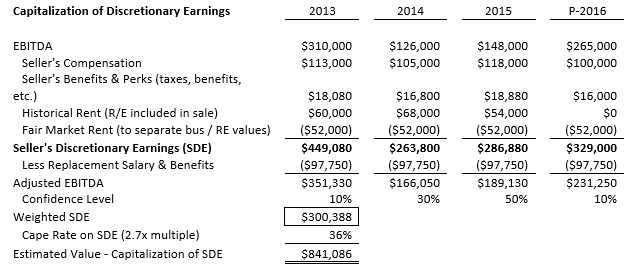

The Role of “Seller’s Discretionary Earnings” in Business Valuation

Typically, “value” from a business valuation standpoint is based on a present value of expected “benefits” to the shareholder…. basic economics in terms of “risk” (cap/discount rate) vs “reward” (benefits or cash flow). Below is a crash course on how cash flow impacts business valuation.

Type of Statements Used. In some cases, “tax returns” are not in GAAP accounting and are not the most accurate reflection on the company’s performance. Relying on cash based accounting or tax returns with tax adjustments can severely over or under value a business; therefore, GAAP financial statements (or the most accurate available) should be used. This is even true when valuing business for SBA lending.

Calculation of Seller’s Discretionary Earnings (SDE). Smaller businesses are typically acquired based on a level of “SDE”, which is calculated as EBITDA + officer compensation + officer benefits & “perks” + or minus non-recurring or non-operating expenses/revenue. This calculation does not take into consideration a replacement salary. Some may say, “we won’t add these back because we’re assuming the potential buyer will also expense his/her auto, benefits, taxes, etc.” However, from a business valuation standpoint, any “benefit” to the owner that’s paid by the company should be included in discretionary earnings.

Properly Weighting Cash Flow. In determining “internal values” for brokers, a standard weighting is typically used. However, if using historical performance to gauge future performance, the weighting should be based on the most reasonable indicator of future performance. For instance, if the Company performed a one-time project in 2013 (or any year) that was not typical in a normal year, why would any weight be put on this year? My suggestion is to give a “confidence level” in % for each year analyzed and how likely the business will perform at that level. There is no right or wrong answer, it’s how you support your final weighting.

Cap / Discount Rates on SDE. Most “mainstream” or small businesses (non-professional practice) will sell in the 2.5x to 3.0x “discretionary” cash flow range. Therefore, cap rates (if inverted) would range from let’s say 30% to 40%. From this range, the analyst should increase or decrease the percentage based on marketability factors such as quality of financial statements (number of add-backs), customer/supplier risk, reliance upon management, growth/margins, pool of buyers, among other factors.

Putting it all together. As shown on the following page, we’ve shown you a straightforward approach to using discretionary earnings to estimate the value of a small business. There are cap / discount rates on EBITDA (and other financial variables); however, discretionary earnings multiples are prevalent and is typically an “apples to apples” comparison because replacement salary is not a consideration (and can be subjective). Our rule of thumb is focus on SDE where there is an owner/operator present and total SDE is below $500,000. For larger businesses where an investor could hire a CEO and/or total SDE approaches say $750,000 or higher, EBITDA multiples are primarily used.

There are multiple levels of “cash flow”; however, discretionary earnings are the most popular to “capitalize” for small businesses. Although some brokers typically focus on “EBITDA” (cash flow after using a replacement salary), next time try the calculation above. Feel free to contact us for “rules of thumb” or comparable sales.

Steven A. Mize, is the Managing Partner at GCF Valuation, Inc. and PeerComps, Inc. Steve is an accredited Senior Appraiser with an extensive background in the business valuation. Please feel free to contact him with questions on this article or with any other business valuation questions.

Upcoming IBBA Learning Webinars

Differentiation & Game-Changing Simplicity: How Verbal Branding Drives Performance & Unifies People

March 2, 2017

12 pm EST

Join Stephen Melanson, founder of Melanson Consulting as he discusses how simplicity modeling allows firms to simultaneously differentiate in the market, unify any number of people, and use Simplicity as a game-changing business tool. The secret sauce is called Verbal Branding™. Unique on the global market, this is the newest (and easiest) way to grow the value of an organization – in all its forms – and make it more ‘sell-able’. And the verbal branding approach represents a fundamentally better way to overcome ever-growing complexity and rapidly solve problems of strategy, sales, and operations.

The questions are, what business imperatives do you need to conquer and, can you unify people around the solutions and continuous improvement?

The Power of the Inbox – Tips and Tricks for Successful Email Marketing

April 12, 2017

12 pm EST

What is the first impression you give when someone sees you in their email inbox? And when they see you there, what do they do?

This powerful webinar takes you step-by-step through the keys to effective email marketing:

- What it really is (and isn’t)

- What it can do for your business

- And the five easy steps you must take to harness the power of the inbox!

Growing a healthy list

Creating great content

Customizing a mobile-friendly template that matches your brand

Getting your emails opened

Tracking your results

From revealing why regular email doesn’t work, to insider tips and techniques like automated list building tools and the design elements that work (and those that don’t!), this webinar will give you the keys to the most effective marketing you can do: email marketing.

Lifetime CBI and Lifetime CBI Retired Requirements Updated

Many members aspire to be awarded the Lifetime CBI and Lifetime CBI Retired. This article will update you on the current requirements and associated benefits of each.

To qualify for the Lifetime CBI award members must now be IBBA members in good standing for 15 consecutive years and maintain their CBI designation for 12 consecutive years. The two periods do not need to run concurrently. Lifetime CBI’s continue to pay annual membership dues and recertification fees, but are not required to attend conferences or participate in ongoing continuing education for recertification.

To qualify for the Lifetime CBI Retired award members must meet the Lifetime CBI requirements and be completely retired from all compensated business brokerage activities. Lifetime CBI Retired has no annual membership dues or recertification fees and are not required to attend conferences or participate in ongoing continuing education for recertification.

Be sure to continuously maintain your membership and CBI in good status to qualify for this prestigious award.

Thanks,

Jeff Snell, M&AMI, CBI, ABI

IBBA Credentialing Committee Chair

ENLIGN Business Brokers

New Member Section

Welcome to our new Members of the IBBA family!

Gaurav Agarwal

Rob Amerince

Kevin Anderson

Russ Anderson

Jim Beno

Steve Bragg

Tom Buckley

Anthony Caliendo

Winchell Chung

Linn Crader

Andrew Cross

Keith Dean

Tracey Deuschle-Burke

Carrie Duvall

Jim Eaton

Brent Engelbrekt

Steven Eschbach

Robert Faus

Yuliya Gaukhman

Kara Gibson

William Goss

Conrad Greene

Donna Greslo

Ryan Heckman

Elizabeth Hirsh

Alison Hoffman

Krista Jenkins

Kimberly Jones

John Kelly

Michael Kelner

Ricky Kerns

Christina lazuric

Robert Lowe

Steve Mccarty

Conor McNaughton

Sylvain Perret

Peter Picciano

Tanya Popov

Faizur Rahman

William Reader

Bob Rizzuto

Loyd Robbins

David Routzahn

Carmen Saad Hanna

Andrew Saikaley

Mitra Sani

Adam Schatzmann

Cortney Sells

Dale Shepherd

Andrew Shepin

Steven Silcock

John Smith

Jason Somerville

Joel Steward

Herb Stewartson

Marc Theeuwes

Jorge Valcourt

Kimberley VanDelinder

Tim Varney

Craig White

[/columns-container]

Get Connected to the IBBA!

IBBA Magazine

IBBA Magazine