IN THIS ISSUE:

LETTER FROM THE CHAIR: IBBA CODE OF ETHICS

As 2019 winds down, I am very proud of the many accomplishments the IBBA has achieved over the year. From record participation at the annual Conference, to new education and new benefits, it’s been a great year for the IBBA and our now 1,400+ members!

As 2019 winds down, I am very proud of the many accomplishments the IBBA has achieved over the year. From record participation at the annual Conference, to new education and new benefits, it’s been a great year for the IBBA and our now 1,400+ members!

Today I’m going to share with you another IBBA 2019 accomplishment which affects all of us as members and professionals in the business brokerage industry: Ethics. Specifically, the IBBA Code of Ethics.

This year your Board of Governors formed a task force to review and update the Code of Ethics.

Of special note is the addition of language that addresses how we represent ourselves and our firms (and franchises where appropriate). Specifically, Article 4 now includes “Business Brokers must not make false, misleading or exaggerated claims about themselves, their firms, franchisors (where applicable) or their competition.” This may seem obvious, but let me give some specific examples. Is it okay to send 2,000 letters to a list of business owners that states “We have buyers for your business”? Probably the most commonly used marketing line in our industry, but it is not a factual statement when sending to a bulk list. I would suggest that if you actually have a buyer that has signed a buyside agreement with you and you have identified a potential target that you call the target and tell them you have been retained by a buyer that is specifically interested in acquiring a business similar to theirs – don’t send bulk messages with broad claims that can’t be supported with specifics. Another example in direct mail or email would be implying that you or your firm have sold “similar” businesses to theirs. This is not acceptable unless you have researched every recipient’s business and cross referenced with a list of businesses that you or your firm have actually sold. Most business owners don’t even know our industry exists. It is not necessary to make claims that test the boundaries of ethical conduct.

Of equal importance is the addition of Article 5 which states “Business Brokers must encourage customers and clients to seek the services of qualified attorneys, accountants, or other professional advisors when applicable. Unless appropriately licensed, Business Brokers must not undertake to provide professional services requiring licensure including, but not limited to legal, accounting, tax, financial planning, and/or real-estate where doing so would be a violation of law in the jurisdiction in which the broker(s) practice(s).” This was specifically drafted to address brokers not providing professional services without the proper licenses as required in the local jurisdiction. It doesn’t matter if you are being compensated or not, no license = don’t do it. Specific to legal services, most states consider providing buyers and sellers template forms as practicing law without a license which is a felony. Unless your state has approved specific buyer and seller documents for use in business transactions in your local jurisdiction, it is an ethics violation to provide legal advice, forms or language to clients – EVEN IF the forms were provided to you by a licensed attorney or a franchisor, and even if you aren’t being specifically compensated for doing so. Leave the lawyering to the lawyers. I tell my clients that second only to my fee, the legal fees are the best money they can spend.

Please take a moment to review the complete updated IBBA Code of Ethics. If you have any questions or concerns please feel free to contact IBBA staff or myself.

Wishing you Happy Holidays and a prosperous 2020!

Jeff Snell, CBI, M&AMI | Enlign Advisors | [email protected]

ADMITTING TO ONE’S ERRORS

Written by Lou Vescio, CBI, M&AMI

After successfully completing the sale of a business that carried over $1 million in inventory, several key lessons were learned. I should mention that it took about 2 years to sell this business, and it should have sold much sooner as we had many good and interested prospects.

After successfully completing the sale of a business that carried over $1 million in inventory, several key lessons were learned. I should mention that it took about 2 years to sell this business, and it should have sold much sooner as we had many good and interested prospects.

Lesson One: Never assume the seller or his bookkeeper understand how to properly calculate Cost of Goods Sold (COGS) on interim income statements. We all know COGS = Beginning Inventory plus Purchases minus Ending Inventory. Easy enough! But the problem stemmed from the fact that the company had a very good inventory system to track products, but they used QuickBooks for their accounting. This resulted in several days lag time from when the product was actually sold to when the sale was recorded in the accounting program, causing the COGS to be consistently overstated. Typically, a few days would mean nothing, but when you sell $40,000 to $50,000 of product per day, and you have a 4-day lag period, the bottom line is impacted by $160,000 to $200,000. At a 4 times EBITDA multiple, that is a significant number. (Keep in mind that a distribution business may only have an EBITDA in the 8-12% range.)

In all fairness to their CPA, he did the proper calculations for the tax returns, but it was well into the selling process. After having lost several good buyer prospects regarding the COGS issue, we finally understood the error in their process regarding interim statements. Convincing the bookkeeper, who was also the wife and part owner, to change her process was a bit touchy.

Lesson Two: For large inventory businesses, the Broker needs to fully understand the process of booking the sale and booking the associated expense. If the company uses an integrated inventory and accounting program, this is not difficult, but we are dealing with small business owners that do not always follow standard processes or have the best software. In hindsight, I should have tried to convince the seller to upgrade to a combined system and wait a year before selling, because I believe he would have had a better insight into his business and would have been more profitable. This could have also increased the final EBITDA multiple.

Lesson three: In family owned businesses, it can be difficult to get the owners to change processes. In this case the husband was afraid to confront his wife regarding her accounting procedures. For 18 months, we knew there was a problem, but getting the husband to talk to his wife about her bookkeeping was not in the cards. It was only after losing some good buyer prospects that the issue was accurately discussed and resolved.

The error was my fault as the broker and not that of the owners. As the broker, I should have identified the problems I described in Lessons One and Two above and discussed these issues with the husband and wife before taking the engagement. Just because the business handled over $10 million in sales a year, it was still a small family owned business. The owners made a very good living from the business, and for their purposes, accurate interim and trailing twelve-month financial statements had little value. On the other hand, the accuracy of the financials was very important to the buyer and his banker, and the selling process was impacted.

After being involved in over 200 transactions, I continue to realize that there is so much to learn about our profession and never enough time. By exposing my error to our members, I hope it helps one or more of you prevent a similar situation.

The good news is that the business finally sold, and we collected a very nice fee.

Lou Vescio, CBI, M&AMI | Coastal Business Intermediaries & Agency Brokerage Consultants

[email protected]

WHY DON’T BUSINESSES SELL?

Written by Lisa Riley, CBI, CBB, PhD

Unrealistic Expectations

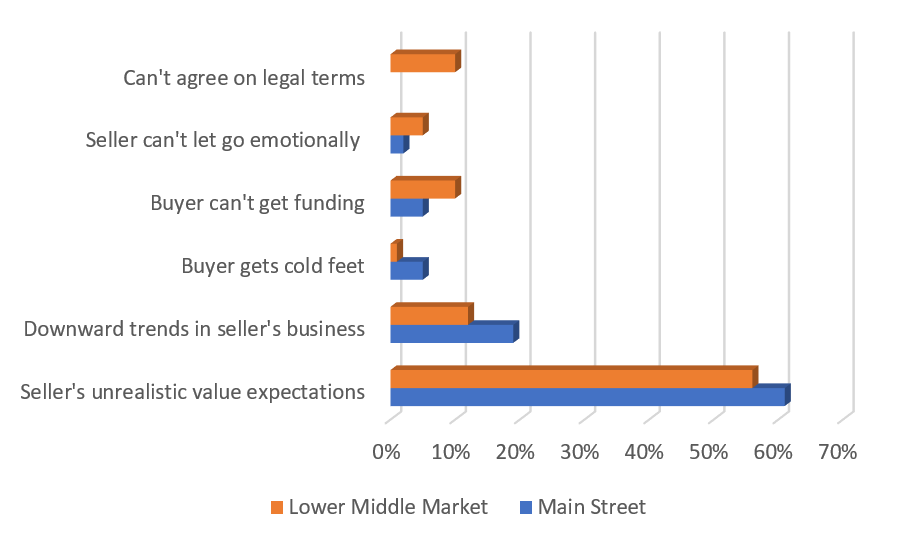

Since beginning the quarterly Market Pulse report in 2012, Advisors have unfailingly reported that the number one reason that businesses do not get sold is that Owners think their businesses are worth much more than its realistic market value. This holds true for both Main Street Business Owners and Lower Middle Market Owners.

For Q3, 2019, Figure 1 shows that almost 2/3 (61%) of Main Street deals fail to sell due to unrealistic value expectations by the Seller and just over half (56%) of the Lower Middle Market businesses.

Figure 1: #1 Reason Businesses Don’t Sell

Although there is much discussion about the reasons for this inflated belief in value, three explanations rise to the top:

- Pride in one’s business (“I’ve spent my life building this business”),

- Lifestyle – amount needed for future (“My lifestyle requires X”),

- Hearsay – (“My neighbor received a multiple of x times).

Regardless, the underlying reason appears to be relatively simple: without an understanding of the market and a plan for exiting, a Business Owner does not know or understand the value.

It is our (Broker/Advisor) responsibility to educate Owners, wherever we meet them along the path. When advisors make unrealistic promises or agree to take a business to market, knowing the seller’s target price is unrealistic, more often than not, the business lingers on the market, the seller’s energy wanes, and business value starts to erode. Advisors who agree to shoot for the moon are really doing their clients a disservice in the end.

By having conversation about what it would take to meet their valuation goals, the Business Owner can decide whether to exit now at a lower value or implement longer-term changes that would add value to their business. Additionally, educating Owners on alternative deal structures, such as earn outs or management contracts, may help bridge the valuation gap and lead to realistic Seller Expectations.

Lisa Riley, CBI, CBB, PhD | LINK Business-Phoenix in AZ | [email protected]

WHAT “SHOULD” BE INCLUDED IN SDE?

Written by Steve Mariani

No matter how you describe the cash flow of a listing, SDE, SDCF, EBITDA or whatever, one thing usually remains the same, there’s add backs and explanations to accompany that and included in those numbers.

No matter how you describe the cash flow of a listing, SDE, SDCF, EBITDA or whatever, one thing usually remains the same, there’s add backs and explanations to accompany that and included in those numbers.

Over the years I have written many articles and conducted many workshops around exactly what add backs are considered by lenders as acceptable when reviewing an offering memorandum. Today I will explain the talk our firm has with every buyer surrounding this particular part of a memorandum. We’ll start by first saying we don’t ever disagree with broker add backs and we never contradict them, EVER! Here is how we start our conversations with buyers: let’s look at the add back items individually to determine what we can provide directly to an underwriter and what we cannot. Many items in that “grey area” are items beyond our level of expertise when deciding if these are IRS acceptable or not so we typically start and focus on items we know will be accepted by a loan officer. That being said, as we work through our due diligence on any transaction, many times along side a potential buyer, we explain that these other add backs that may not be accepted are still critically important to cash flow and just ones we cannot consider as lendable debt service cash flow.

If you haven’t heard the lender “unwritten rule” then I will share a lending secret here today. If more than 20% of the SDE or cash available is coming from add backs then it raises flags and causes a deeper look into much of the financials. Included in the 20% is NOT owner’s salaries, interest, depreciation and the like of acceptable add backs, this is not what’s in question here. I’m referring to things like the home groceries purchased with a company credit card, the children’s nanny or sometimes its as big as the entire home mortgage run through expense line items. Items that I am not qualified to determine are “Blatant IRS Fraud” but many lenders are trained to determine and by exposing a seller to them could be trouble. Not only for our loan request but on a higher level. SBA lenders have the responsibility of exposing blatant fraud directly to the IRS, something many people are not aware of. So, the question truly becomes, do you include these in your listing and cash flow or leave them out and explain it to each potential buyer. The answer is simple, keep doing what your doing and know who your exposing that offering memorandum to, from a lending perspective. If your presenting an OM that includes many of those blatant items to a new or unfamiliar lender be careful of the outcome, I’ve witness this in person and the outcome is not something any of us want to be part of.

Your options regarding a listing with many blatant concerns may be to set seller expectations a little differently. Determining if financing is available for this business may be one of them, maybe it’s best to consider all seller financing or possibly a lower asking price. This is where the broker’s expertise really comes into play and knowing how to address these potential concerns becomes top priority, many times before the listing agreement is even executed. Each broker office operates differently, but we know of many broker offices that will not accept a listing if provable and documentable cash flow by itself will not support the asking price. I am in no way suggesting this become a standard practice for your office but understanding this and determining to what level and amount of add backs your comfortable including is a decision you alone can make.

Before any OM leaves our office, we have completely reviewed each and every item included in the overall cash flow of the business. We’ve calculated the documentable add backs and our debt service coverage ratios for the last 3 years and have determine which to present and what questions might arise from presenting them. It’s all about no surprises in our lending industry. Meaning, if underwriting exposes something we missed or neglected to include, shame on us, its our job and what we’re getting paid to do as the experts. This doesn’t mean you have to go to the lengths that we do, but the more you do and understand the easier your getting to an approval. What we never want is the alternative to an approval which is just not acceptable here in our offices.

Once SDE has been determined from a lenders perspective and we’ve completed our internal due diligence on this business, we will then inform the buyer of our outcome as we apply for the financing. Aside from sharing what we’ve determined, we will also always point them toward the items we did not include in our calculations and explain that these items are of high importance and usually easily verifiable by them. We’re always very specific when explaining to a potential buyer which add backs we did not include and why, along with the information to allow him or her to research and reach their own conclusion. Bottom line, to answer the actual question above, we always recommend a broker include all available cash flow and should adjustments need to be made, we’ll suggest them as we work through the transaction.

If this business has previously secured a lender pre-qualification letter, then they should have already completed the due-diligence and will just be adding and reviewing the buyer’s personal information. This practice saves countless hours and days while moving toward a closing on any project.

Steve Mariani |Owner of Diamond Financial Services | [email protected]

IBBA BEST PRACTICE SERIES: PREPARING FOR THE FIRST BUYER-SELLER MEETING

Written by Randy Bring, CBI

Great job! You’ve listed a profitable business; you’ve advertised the company and are now receiving some quality inquiries from potential Buyers. Successful Business Brokers understand the critical importance of the first meeting between a Buyer and a Seller and that one of the most important functions a listing Broker can perform is to properly prepare his or her Seller for this meeting.

With the assumption that the Buyer prospect has signed an NDA and has received a basic write-up on your listing, an appropriate next step will likely be a face to face Buyer-Seller meeting or, possibly an introductory conference call with the Buyer, Seller and the Broker(s) involved. Planning for this meeting with your Seller can assure a successful “first date” leading to sustained interest from the Buyer and deal progression. So how do you take control of this important step in the sale of the business?

Read the full Best Practice Article through your member portal at mywww.ibba.org!

Randy Bring | Transworld Business Brokers, Inc. | [email protected]

UPCOMING 2020 IBBA CONFERENCE – SAVE THE DATE

The 2020 IBBA Annual Conference will be held in Louisville, KY on April 24 & 25! Registration will open in January 2020, so be sure to register to join us for The Marketplace, Workshops, Masterminds, Awards Program, Courses and more!

GET EVENT DETAILS HERE

IBBA Member Benefits – Just Added V-Rooms!

To get started with your FREE access, login to your IBBA Member Account to get access from each benefit partner:

Bizminer

Business Reference Guide Online

ValuSource

V-Rooms

Get Connected to the IBBA!

IBBA Magazine

IBBA Magazine